Location: Home >> Detail

J Sustain Res. 2021;3(1):e210006. https://doi.org/10.20900/jsr20210006

Institute for Environmental Sustainability, Mount Royal University, 4825 Mt Royal Gate SW, Calgary, AB T3E 6K6, Canada

* Correspondence: Connie Van der Byl.

This article belongs to the Virtual Special Issue "Corporate Sustainability"

Background: Globally, governments are responding to climate change. The financial industry has followed, integrating climate risk to their investment decisions via Environment, Social and Governance (ESG) considerations. Firms in environmentally sensitive industries, like oil and gas, are notably scrutinized for their ESG performance especially regarding climate change.

Methods: Two samples were selected for a content analysis and comparison of environmental disclosure and investor requirements. The first sample is comprised of the sustainability reports for 30 oil and gas firms operating within Alberta. The second sample includes the ESG reports of 19 financial institutions with investment in the oil and gas industry. This data was triangulated via fieldnotes from conferences and informal discussions with oil and gas and financial industry representatives.

Results: We find that both ESG investor requirements and firm disclosures suffer from a lack of standardization. Consequently, the financial industry is moving toward the adoption of the TCFD (Task Force on Climate-related Financial Disclosures) recommendations and the SASB (Sustainability Accounting Standards Board) framework in firm evaluations. European financial institutions have been leading the way in requiring firms to define their climate risk, set targets, measure performance, show improvement, and connect to strategy. Alberta oil and gas companies are responding with more robust ESG disclosure, though SASB and TCFD reporting is not yet widespread.

Conclusions: Industry failure to respond to evolving disclosure requirements can lead to divestment. We contend that oil and gas companies that do not acknowledge climate risk and outline energy transition strategies tied to their business models and reputations potentially sacrifice access to capital. We expect firm ESG disclosure, especially radical transparency on environment, to increase as financial institutions execute on climate change risk evaluations. We contribute to the sustainability reporting and ESG literature by showing the impact of investors as stakeholders in effecting change to oil and gas firm level environmental disclosure.

ESG, environment, social, and governance; GHG, greenhouse gas; GRI, global reporting initiative; MNC, multinational corporation; TCFD, taskforce on climate-related financial disclosure; SASB, sustainability accounting standards board; IPIECA, International Petroleum Industry Environmental Conservation Association; CDP, carbon disclosure project; UN, United Nations; CAPP, Canadian Association of Petroleum Producers

Environment, social and governance (ESG) considerations are now part of conventional financing decisions. In the past, consideration of nonfinancial risk was the realm of impact and ethical investors. Now, all global financial institutions are issuing ESG reports that disclose their impact and also map out criteria for making investment decisions tied to ESG. For environmentally sensitive sectors like mining and energy, the E in ESG is critical. The energy sector is vulnerable to the physical impacts of climate change such as increased demand for electricity, water scarcity, and infrastructure damage from catastrophic weather events. In addition, governments around the world are developing measures to lower country-level GHG emissions that directly impact the energy sector [1].

Climate change is a grand challenge of our time [2]. The COP21 Paris Agreement in 2015 was hailed as an ambitious goal that signaled nations around the world as taking climate change seriously. The universal agreement aimed to limit rising temperatures due to climate change to an increase of 2 degrees Celsius globally and to strive to cap that rise to 1.5 degrees Celsius. Committing to reducing emissions within their borders requires changing technologies, cultures, ideologies, and policies. The shifting political context will affect corporations and industries. Most recently, the financial community has embraced consideration of sustainability, and in particular climate change.

To address the grand challenge of climate change significant reductions in GHGs are needed. Many call for an end to fossil fuel production. While gains are being made in alternative energy production and commercialization, the shift away from fossil fuels use will not be immediate. It is important, therefore, that as long as the world needs fossil fuels, that they be produced with the least environmental impact possible. Increased financial institution requirements for improved environmental performance, including addressing climate change, could have impact on the oil and gas industry especially given increased challenges in accessing capital. Our research examines this proposition and asks the following questions: Are financial institutions requiring more of oil and gas firms in terms of environmental performance, especially in their response to climate change? How are oil and gas firms responding? Does firm level disclosure align with investor requirements? Financial institutions acknowledge and, in some cases, develop processes for evaluating climate risk. This interest was initially spurred by Bank of England Governor Mark Carney and Michael Bloomberg in 2016 [3]. Since then, the highly influential CEO of Blackrock, Larry Fink, has published letters urging organizations to consider ESG factors while highlighting the impact of climate change on financial markets and firm performance [4]. While concern for our planet is a factor in this shift, investors also clearly identify the link between climate risk and financial risk.

Understanding the current requirements of financial stakeholders is an important consideration in the pace of industrial decarbonization. The current regulatory environment in Canada has left ESG disclosure as a non-financial disclosure not required by law. The voluntary nature of ESG disclosure creates large variation between firms and raises concerns as to whether firms will make substantive progress on improving environmental performance given the lack of consequences for poor performance [5]. However, this view ignores the significant impact financial institutions can have on firms in the form of restricted access to capital and investment [5]. We address this gap in the extant literature using a content analysis of Alberta oil and gas company sustainability reports and financial institution requirements.

We examine the sustainability reports of 30 oil and gas firms in Alberta, Canada. Our sample represents firms of various sizes and resource specificity. Coders evaluated the reports for standards applied, metrics, narratives and overall quality and intent. We then analyzed the ESG reports of 19 global financial institutions to determine their requirements for investment generally and more specifically for the oil and gas industry. We define gaps in reporting and requirements and observe improvements and continued challenges in sustainability reporting that should be addressed.

The investor emphasis on ESG and climate risk has caused firm-level sustainability reports to garner more attention and importance. The literature on sustainability reporting, and more recently ESG, points to deficiencies in consistency and comparability of information. While frameworks like the Global Reporting Initiative (GRI) and now the Sustainability Accounting Standards Board (SASB) aim to provide guidelines, their adoption and successful implementation vary [5].

We find that heightened interest by global financial institutions in climate risk leads to requirements and expectations in sustainability reporting that begin to resemble standardization. Further, we show that firms are responding to the ESG requirements of investors to varying degrees. We contribute to the growing ESG management literature by highlighting the impact of investors in driving ESG performance. This extends research that shows how reporting influences investment decisions. We also contribute to considerations of stakeholders by highlighting the importance of investors and their ability to effect change in ESG considerations by firms. In this way, we expand the literature on sustainability reporting and ESG disclosure, and we provide practical insights to both oil and gas firms and financial institutions.

Sustainability ReportsSustainability reports have been given many names: corporate social responsibility, corporate responsibility, triple bottom line, and corporate citizen reports, among many others [6]. Daub [7] defines a sustainability report as a report which “must contain qualitative and quantitative information on the extent to which the company has managed to improve its economic, environmental and social effectiveness and efficiency in the reporting period and integrate these aspects in a sustainability management system.” Sustainable business practices in and of themselves are insufficient to increase awareness and legitimacy for the firm. Reporting of those practices is needed [8].

The connection between sustainability practices and corporate reputation or firm legitimacy has been well developed in the literature [9–11]. The value enhancing aspect of reputation is further connected with market or financial return [11,12]. Thus, strong disclosure leads to improved reputation which translates to higher profitability or access to capital. Of course, the opposite is also true where poor disclosure can lead to skepticism and a reputation for “greenwashing”. Various frameworks have been developed to provide guidance and standards for voluntary reporting to mitigate the risk of misrepresentation.

FrameworksThe GRI has been the standard for sustainability reporting since the late 1990s when it was developed by non-profits with support from the United Nations [13]. The goal of the GRI is to create a transparent global governance system encouraging accountability on sustainability metrics. The practical value of the GRI is in guiding voluntary disclosure across multiple dimensions. However, adherence to GRI requirements may create barriers to its adoption. Where requirements are more open to interpretation and customization, comparisons become difficult [14]. Stakeholders may have challenges comparing reported performance across companies given inconsistencies and variations in approaches and assumptions [15]. Striking a balance between stringency and diffusion of the framework seems elusive.

As climate risk and financial interest in disclosure has increased, the TCFD (Task Force on Climate-related Financial Disclosures) recommendations and SASB (Sustainability Accounting Standards Board) framework have emerged as preferred. In early 2020, one of the world’s largest investment advisory firms, Blackrock, advocated for standardized use via the CEO’s annual letter to investors. The TCFD guides climate related financial disclosures to the benefit of investors, companies, lenders, and insurers. SASB aligns with the TCFD in assessing material risks. The SASB framework provides industry specific guidelines for climate risk and materiality disclosure [1]. As Eccles and Krzus [16] contend, “simply put, the TCFD is asking companies to report on their response to the risks and opportunities created by climate change”.

Many firms are also including the United Nations Sustainable Development Goals (UN SDGs) in their sustainability reports. These 17 goals were developed in 2015 and envelop the grand challenges of our time including climate change, poverty, diversity, energy, consumption, Indigenous rights and more [17]. The UN SDGs provide an opportunity for the private sector, especially large multinational corporations (MNCs), to engage in global social issues [18]. Shell Canada produced one of the first environmental reports in 1991 [19] and the company continues to progressively report on ESG performance with the inclusion of UN SDGs. In a review of annual reports by the UNGSII Foundation [20] 89 percent of 100 analyzed blue-chip companies explicitly or implicitly referred to the SDGs in their 2017 annual reports.

Disclosure QualitySustainability reports vary in quality and meaningfulness to their audience [10,21]. Dawkins and Lewis [22] surveyed 93 analysts, 50 investors, and 30 journalists and found that 45, 54, and 63 percent, respectively, think that disclosed information on corporate sustainability performance is of poor quality. Companies in Europe are typically further along in their attempts to provide greater data transparency on their ESG performance than businesses in North America [23].

Inconsistency in reporting metrics and approaches, and challenges in comparing firm performance occurs in most sectors [24]. In addition, there is the potential for companies to disclose only positive information to support their image while ignoring negative impacts [14]. Third party assurances have been used to increase credibility [9,21,25]. De Villiers and Van Staden [26,27] examined the attitudes and requirements of shareholders toward corporate environmental disclosure. They found that shareholders are positive about the disclosure of environmental information but want such information to be made compulsory, to be audited and to be published both in the annual report and on the company website.

Inconsistency in data extends from between firms and industries to within a single firm. For example, the Carbon Disclosure Project (CDP) is a channel for reporting GHG emissions. Depoers, Jeanjean and Jerome [28] find that firms may decouple CDP disclosure on GHGs from numbers published in corporate reports. This may be accomplished by excluding scope 3 or downstream/end-user emissions in the corporate report or by changing the sources of emissions. And so, firms apply their own standards in corporate reporting and depart from the CDP requirements.

Environment, Social, and Governance (ESG)The relatively recent proliferation of ESG assessment into conventional investing has occurred as climate change and associated investor concern has increased. Previously, socially and environmentally conscious investing was captured through tailored and niche ethical and impact investment offerings. ESG investment strategies often include the exclusion of specific firms, concentrating on certain industries, selecting the best firms on ESG performance, activism, and board engagement. Generally, the strongest focus has been on Governance for its direct link to management [29]. There is an expectation that large cap companies will have higher ESG disclosure than mid-cap companies [30].

The academic literature on ESG is growing. One body of research indicates a decoupling between ESG disclosure and ESG performance. Authors argue that ESG performance measures actual firm performance while ESG disclosure represents a communication tool for firms to address stakeholder needs [31,32]. Eliwa et al. [32] found that disclosure can symbolically mask poor substantive ESG performance. In this work, ESG performance is operationalized using aggregate ESG rankings developed by rating agencies. While valuable, ESG ratings pose significant problems for researchers. Generally, rating agencies follow the lead of firms through their disclosures rather than providing objective analysis of ESG performance. In addition, “data aggregators usually have limited access that limits the availability of the data. Moreover, data aggregators limit the company in representing the information according to particular indicators” ([5], p. 9). As a result, there is an opportunity for researchers to assess firm disclosure independently rather than rely on ratings. Subsequently, the extensive information provided in ESG disclosure reports on risk management processes and potential weaknesses [32] can be integrated into the analysis.

Stakeholder theory provides insights to the use of ESG disclosure as a communication tool rather than a reflection of actual performance. Freeman [33] defined stakeholders as groups or people who “affect or [are] affected by the achievement of an organization’s objectives” (p. 46). Researchers have focused on understanding why managers prioritize a particular stakeholder’s concern. A key concern is stakeholder salience or the “degree to which managers give priority to competing stakeholder claims” ([34], p. 854). Managers are expected to place a greater focus on the demands of stakeholders that have greater leverage over firm strategic considerations [34]. Voluntary ESG disclosures can be a method of communication between firms and salient stakeholders [35]. Frooman [36] found that the power stakeholders can exert over firms is directly related to their control over resources necessary to the firm. Therefore, investors are key stakeholders to public companies.

The financial implications of ESG disclosure have been analyzed across multiple dimensions and a sizeable body of literature has emerged. Neu, Warsame, and Pedwell [37] argue that firm disclosure is targeted at financial institutions as they are generally deemed the most important stakeholder to for-profit firms. Studies show that financial institutions use environmental information in determining credit risk [38–40]. Goss and Roberts [41] found that firms with low CSR (now commonly referred to as ESG) performance received a significant premium on the cost of capital.

The primary focus of the ESG literature to date has been investor response to disclosure [5,42,43] and not the impact investors have on firm disclosure and, by extension, ESG performance. Eliwa [32] notes that the power of financial institutions to withhold financing enables them to require greater transparency and disclosure standardization [32]. However, little empirical research has been conducted to determine how firms are responding to the ESG requirements of investors and the impact of investors in driving ESG performance. We address this gap by evaluating the environmental disclosure of 30 Alberta oil and gas firms in comparison to the requirements of 19 global financial institutions.

This study uses a qualitative content analysis methodological framework. Content analysis is a widely used methodological approach in business, communications, and psychology research [44,45]. A significant benefit of this methodology is the inclusion of both qualitative and quantitative aspects. While primarily a qualitative methodology for “identifying, analyzing, and reporting patterns (themes) within data” ([45], p. 6), the capability to also produce numerical summaries of the phenomenon under question provides researchers the ability to gain a greater depth in insights [45]. In our study, we followed the standard format for content analysis set forth by Lombard et al. (2002) and outlined by Neuendorf [44]. Four coders were used to minimize the potential for principal investigator bias, and reliability metrics were calculated (See Below).

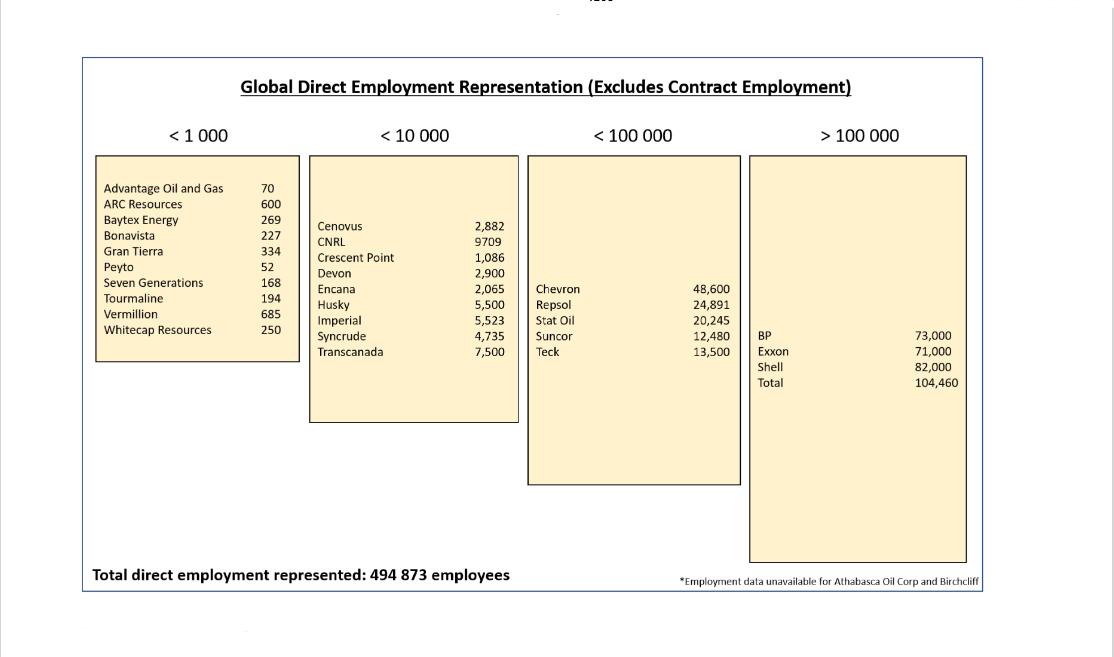

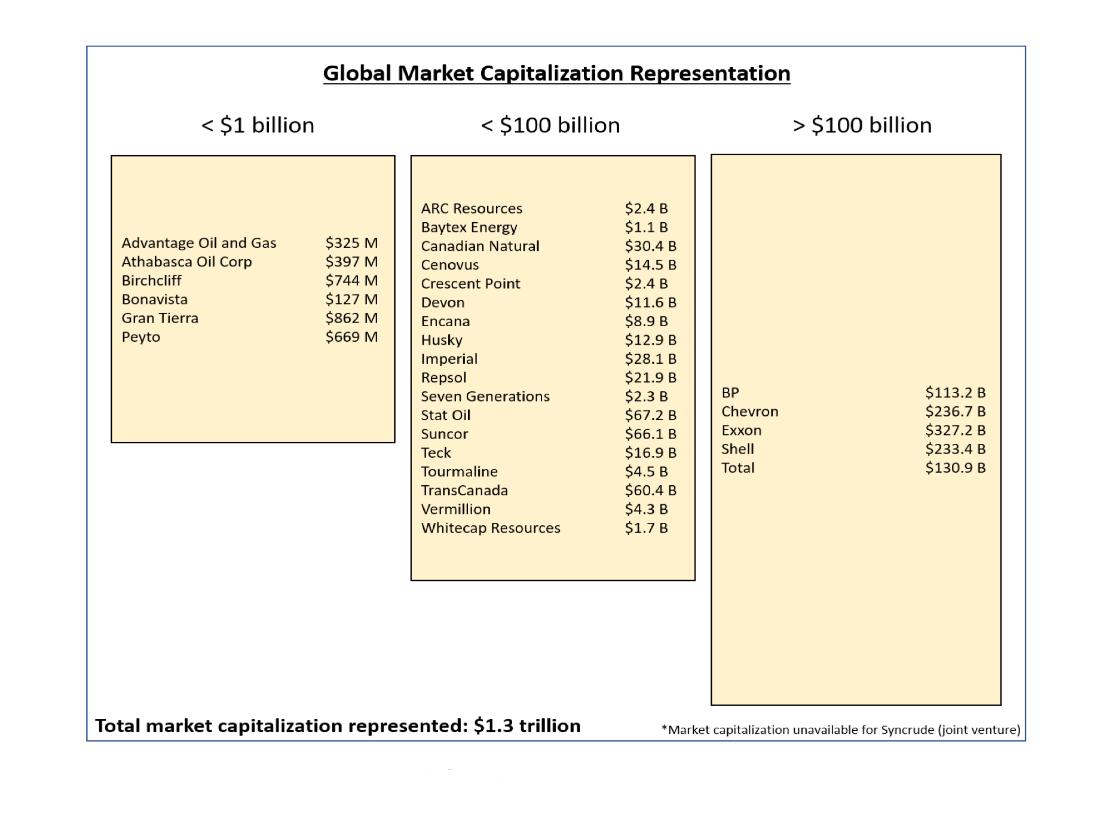

We first evaluated the sample of 30 Alberta oil and gas sustainability reports for disclosure approaches. The oil and gas industry within Alberta is comprised of hundreds of firms. To ensure our sample adequately represented the Alberta oil and gas industry, firms with varying market capitalization (market cap) and production were selected (please see Figures 1 and 2). Companies selected were either headquartered within Alberta or had an operational presence in the province. Half of the sample group comprises firms producing over 100, 000 barrels of oil per day which represents the majority of production within the province. The remaining 15 firms were selected from mid to small capitalization producers. The final sample of 30 companies includes global oil majors, large domestic firms, and smaller provincial producers representing a fair approximation of the Alberta Oil and Gas industry.

Following Braun and Clarke [45] the team engaged in an iterative process to determine the appropriate themes to be coded. The team of four coders assessed the publicly released sustainability reports of selected firms for the year 2017. Initially, sustainability reports for the largest market cap companies in the dataset were evaluated. The large market cap firms were selected as the trial sample since the literature reviewed indicated that large multinational firms have higher disclosure quality and were therefore better suited to capture all potentially relevant codes [44]. The iterative process included both a top-down approach informed by the literature review and a bottom-up approach that allowed for emergent themes within the data to be considered [44,45]. The team compared their codes and developed a standardized guide for the remaining reports. The coders looked for the use of reporting frameworks, external indices and ratings such as the Dow Jones Sustainability Index, and the inclusion of the UN SDGs. Inclusion of firm level sustainability strategies were identified, including whether sustainability and the broader corporate strategy were linked. Key messaging, metrics, and terminology in the areas of land, air, water, communities, employees, and Indigenous relations were identified. The inclusion and scope of external assurance was also recorded.

Formal evaluation using the standardized guide was followed by a brief personal reflection detailing coders’ impression of the overall credibility of the report, effectiveness of the CEO letter, key messaging, and general thoughts on the content and formatting. Coded data were directly compared between firms.

Figure 1. Oil and gas firm employment.

Figure 1. Oil and gas firm employment.

Figure 2. Oil and Gas Firm Market Capitalization reported in USD.

Figure 2. Oil and Gas Firm Market Capitalization reported in USD.

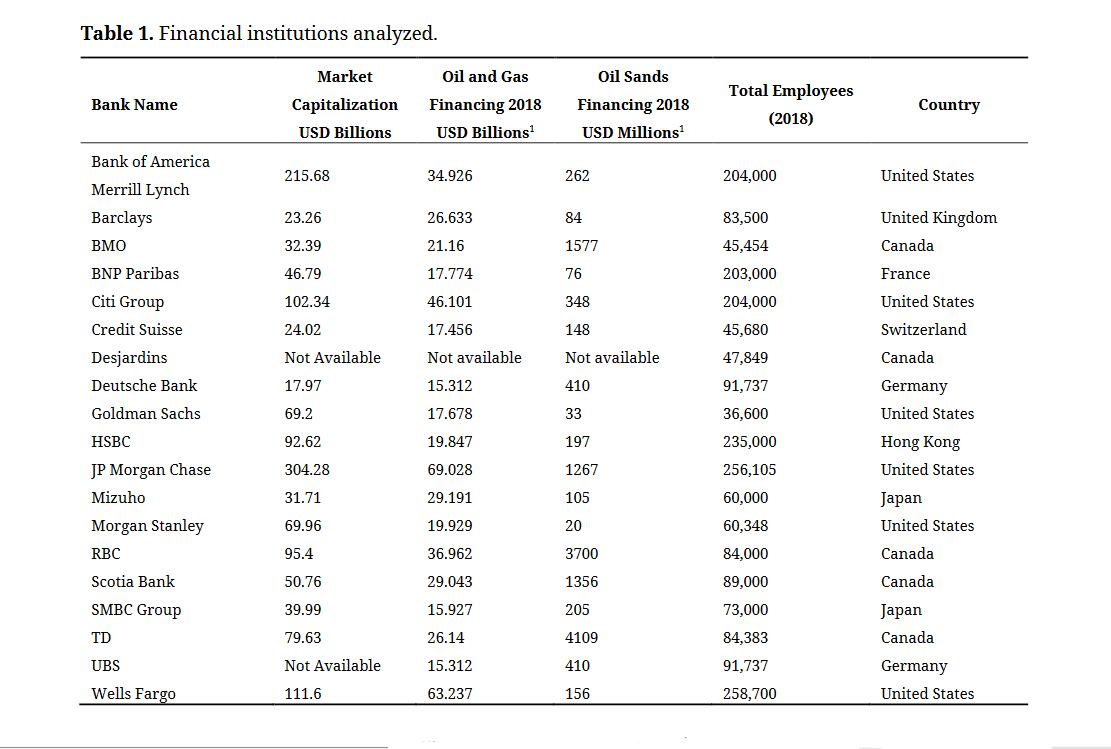

Next, we identified 19 mid to large size financial institutions with publicly released ESG reports. The financial institutions were selected to represent global coverage based on the amount of oil and gas financing provided (see Table 1). Further, the financial institutions selected all provided financing to the Alberta oil sands at the time of analysis. Apart from UBS and Desjardins all financial institutions reviewed are among the top firms financing oil and gas development [46]. The selection of financial institutions represents a wide geographic range, variation in firm size, and both public and private firms. Financial institutions from eight countries were included in the analysis with the greatest concentration in the United States and Canada. The firms selected also vary in the level of financing provided to the oil and gas industry. The variation in the financial institution sample provides a range of firm perspectives across the financial industry and limits the influence of firm size or regulatory discrepancies.

Table 1. Financial institutions analyzed.

Table 1. Financial institutions analyzed.

The coding team again engaged in an iterative process to develop the coding scheme for the financial institutions. However, to ensure that the content analysis would be able to address our primary research question the majority of the themes selected for coding were determined in a top-down fashion by the principal investigators [44]. Specifically, consideration of reporting frameworks and ESG risk management process, use of the TCFD, use of oil and gas transaction disclosures, and requirements for investment in oil and gas were identified. Specific attention was given to how financial institutions assess and manage climate related risks in their portfolios with a focus on the exclusion criteria and metrics used to assess the oil and gas industry. Financial institutions were then grouped based on the individual firms’ specific ESG disclosure requirements.

At this stage, the first author returned to the oil and gas sample to compare for consistency with financial institution requirements. The disclosure requirements identified in the financial institution review were compiled into a standardized form. Metrics assessed included mention of climate and transition risk, mention of climate change, GHG intensity, GHG footprint, use of the TCFD, data reporting consistency, and the use of hard targets for environmental impact reduction. The oil and gas sample was then grouped based on their current ability to meet financial institution disclosure requirements.

A fundamental step in ensuring the reliability of a content analysis is the verification of interrater reliability. Interrater reliability is crucial in establishing that the coding scheme is applicable across researchers and not limited to an expert analyst [44]. To establish interrater reliability Cohen’s Kappa and simple agreement were calculated. Simple agreement is the base calculation of agreement between two coders and does not account for chance. To address the influence of chance in human coding, Cohen’s Kappa is calculated in addition to simple agreement [44]. Following Neuendorf [44] we utilized 0.6–0.8 as the range of “substantial agreement” and above 0.8 as “almost perfect agreement. All variables measured received a kappa above the 0.6 cutoff, with an overall agreement of (Kappa = 0.84) and a simple agreement of (0.92). The high level of agreement is consistent with a content analysis consisting primarily of nominal codes [44]. Due to the limited sample used in our study reliability metrics were calculated using all coded reports in the sample. Based on the reliability tests conducted and the level of substantial agreement between coders these findings are considered reliable, but not generalizable due to the limited sample size [44].

In our engagement with oil and gas industry members, we heard that there was confusion regarding what to report and how. Investors similarly expressed frustration publicly with a lack of standardization in ESG reporting. Our results support these assertions, and we consider the reasons for this obfuscation and the resulting gap between industry reporting and investor requirements. We find that oil and gas firm-level disclosure on the E in ESG varies in degree of alignment with investor requirements. At the same time, while Wall Street and Bay Street place greater emphasis on environmental disclosure, requirements vary across financial institutions. In the following sections, we provide details of the disconnect between what some firms are reporting and what some financial institutions are requiring.

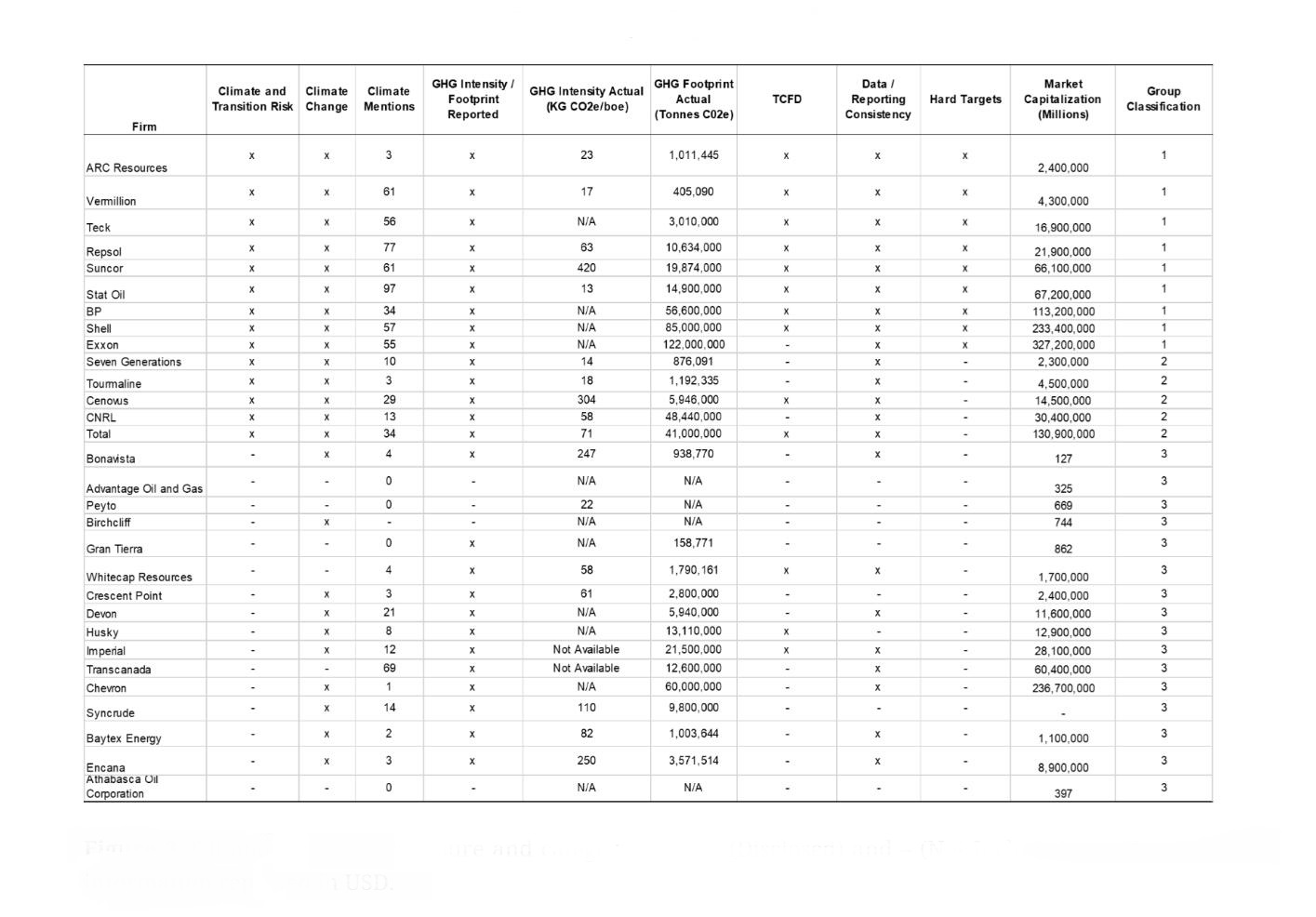

Alberta Oil and Gas Firm Environmental DisclosureWe categorized Alberta oil and gas firms according to their size. From the literature [47] and our exposure to industry leaders, we know that disclosure is linked to available resources within the firm, which may be tied to firm size. As shown in Figures 1 and 2, 15 of the 30 or half of the companies assessed have a market capitalization of over $8 billion and more than 2000 employees. While the large cap firms did rank highly on disclosure, we find similar results for the mid and small cap firms (Figure 3). We further find ESG disclosure variability across all 30 oil and gas sustainability reports analyzed. We classify this variation under the headings of disclosure mechanisms, sustainability strategy and environmental performance metrics.

Figure 3. Oil and gas firm disclosure and categorization. X (Disclosed) and – (Not Included). All financial information reported in USD.

Figure 3. Oil and gas firm disclosure and categorization. X (Disclosed) and – (Not Included). All financial information reported in USD.

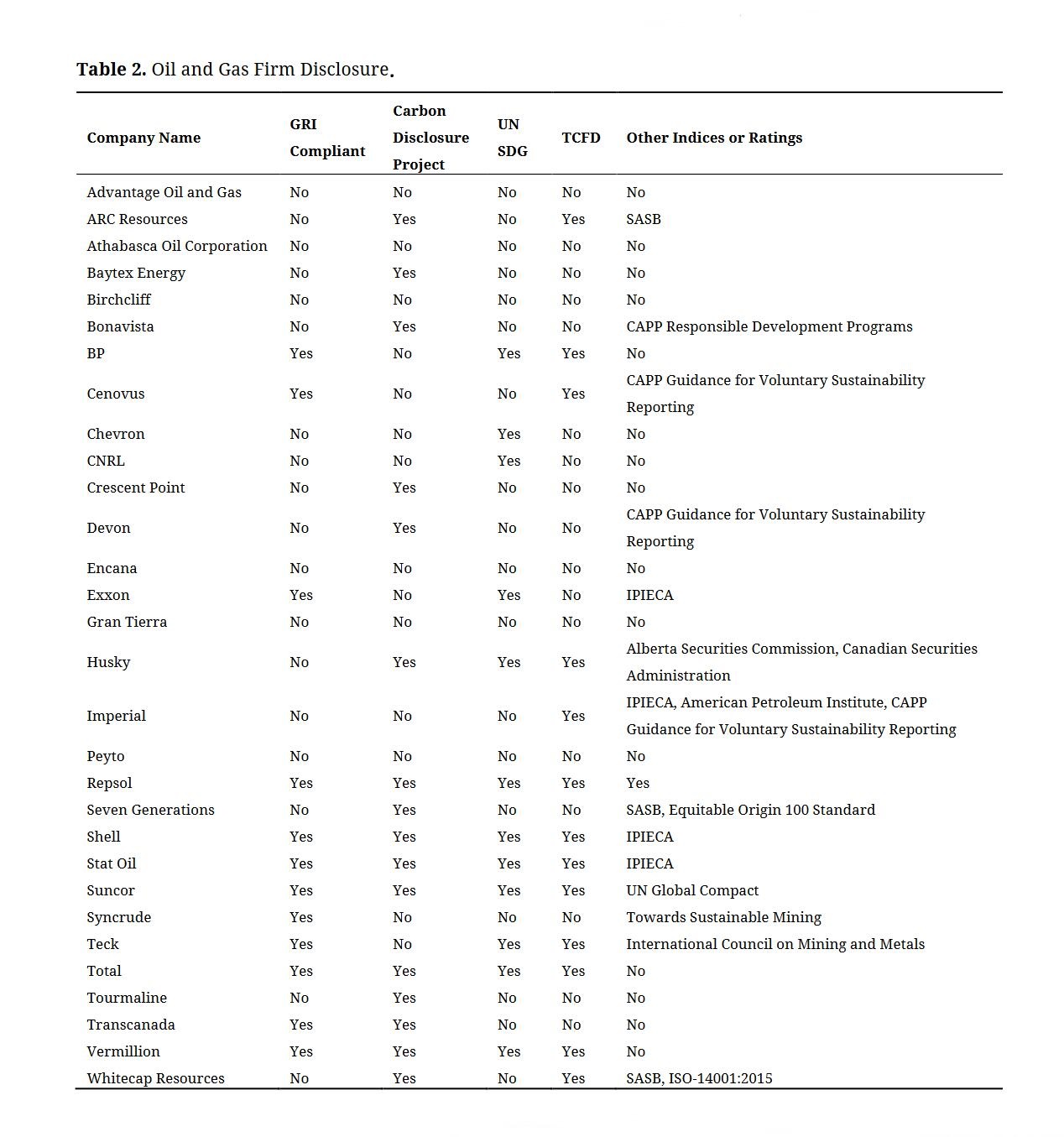

We find variation in the disclosure frameworks used by firms in our sample. More than half of the companies are GRI compliant or informed. A handful cite the International Petroleum Industry Environmental Conservation Association (IPIECA). Only ARC Resources and Seven Generations which are smaller cap (see Table 2) note the use of SASB. Firms with above industry average ranking in the Carbon Disclosure Project (CDP) reported their ranking. As a result, those that mentioned CDP but failed to disclose a ranking are thus open to scrutiny. UN SDGs are referenced by 10 of the 15 large cap firms and 12 of the 15 cite the TCFD. Smaller market cap companies from our sample are not currently integrating the SDGs and TCFD.

The average length of the sustainability reports reviewed was 70 pages with the Suncor report longest at 158 pages and the CNRL report shortest at 28 pages. Encana (now Ovintiv) and Athabasca Oil Corporation did not publish a report but rather used their corporate websites to display environmental performance. Most of the companies in our dataset use third party assurances. These are typically completed by one of the “big 4” accounting firms with Deloitte and PwC most often used.

Table 2. Oil and Gas Firm Disclosure

Table 2. Oil and Gas Firm Disclosure

The GRI framework is widely used among firms. However, many companies cite the framework without being fully compliant, or fully detailing compliance efforts. Reports that directly connected the GRI to specific sections within the report created a stronger impression of following the framework. Despite widespread use of the GRI to “inform” or “guide” reports, the full use of GRI compliance is limited.

The SDG’s were used throughout the sample as a narrative framework to present initiatives and actions. Vermillion’s sustainability report is the best example of integrating the UN SDGs. Every section of the report is connected to an SDG. Further, in sections such as air, projects to reduce emissions are directly tied to an SDG. The use of cross goal connections, that is showing that sustainability initiatives can work across all three aspects of social, environmental, and economic, suggests a commitment to sustainability.

Sustainability strategySustainability strategies ranged from including sustainable development in the corporate strategy statement to complete strategy sections with specific goals and action plans. Most of the large cap firms define their sustainability strategy but few link it to overall corporate strategy. CEO commitment is reflected in the CEO letter. Honesty and transparency were conveyed when the CEO letter directly addressed negative events such as fatalities or failure to meet emission targets. Some CEO letters seemed disconnected from the report entirely as if the CEO were unfamiliar with the report contents. Most were somewhere in the middle, with a fairly general letter but drawing on content from within the reports. The large cap firms have sustainability committees within the Board. The sustainability reports often state the specific responsibilities or guiding principles of the board. While only 50% of the sample analyzed had explicit sustainability strategies, there is a growing acknowledgement of both the risks associated with climate change and the implications of man-made climate change. This growing acceptance among the oil and gas industry is an important change in the conversation around decarbonization. Apart from TransCanada all firms in the top 25% of climate mentions were grouped in category 1 or as responding to all financial institution disclosure requirements. While climate mentions as an isolated metric are neutral, the increasing discussion of climate change is an indication of the growing focus placed on it by the oil and gas industry.

Most firms highlight their Indigenous and stakeholder engagement strategies as well as safety cultures. The emphasis on safety confirms that this is a priority in the industry and is well established. Oil and gas firms have recently prioritized Indigenous engagement in response to project opposition from affected groups. Companies described their engagement with Indigenous groups in a positive light but most often failed to provide any associated metrics or goals. The emphasis on the engagement strategies and certain environmental performance measures, for example, water management, suggests that these issues are well addressed in the organization. However, we then questioned the approach to environmental items that were often less of a focus, for example, GHG emissions. In some reports, GHG emissions were a significant focus, but this varied between reports. Basic water metrics (consumption, etc.) and land metrics like spills were reported somewhat more consistently between firms (i.e., most firms at least addressed these issues in some way).

Climate change strategy was most developed by the large cap MNCs like StatOil (Equinor), Repsol and Shell. These strategies were associated with a more open and transparent discussion of climate change within the report, with emphasis on how oil and gas fit into the new energy mix. This contrasts with companies lacking a specific strategy who did not include or feature such a discussion. Importantly, several of the smaller firms as measured by market capitalization have moved forward with sustainability strategies connected to their primary corporate strategy. As shown in Figure 3, the amount that climate change is addressed varies.

Environmental performance metricsThere is a lack of consistency and standardization in reporting important environmental performance measures related to land, air, and water impact. We find that oil and gas firms reported information over differing time scales (e.g., two years versus five years) making a comparison across firms difficult. Further, the metrics available varied across the sample with several firms failing to disclose common metrics such as GHG footprint. Within metrics disclosed variation was also found primarily in the unit of measurement. For example, GHG intensity is a common industry metric representing the amount of GHG emitted per barrel of oil equivalent produced. The standard unit for this metric is a kilogram of carbon dioxide per barrel of oil equivalent (kg of CO2e/boe); however, multiple firms either fail to disclose this metric or use alternative units. The inconsistency in metrics, units, and time present several challenges in making direct comparisons across the sample. The inconsistency in disclosure metrics is a primary focus of the TCFD and SASB framework which require the disclosure of financially material environmental risks across defined categories.

Firms with the lowest disclosure quality (classified as 3 in Figure 3) are characterized by a lack of consideration for climate risk, no targets for environmental performance, and a low adoption of the TCFD. While these oil and gas firms have begun to acknowledge the potential impacts of climate change, overall mentions of climate change were lowest in the dataset. Despite the lack of consideration given to climate risk most of these firms still disclose their annual GHG footprint often due to regulatory requirements in their home country. We find the highest level of inconsistency across disclosure metrics and data availability among firms that fail to address climate risk explicitly. The inconsistency reduces the ability of financial institutions to quantify the risks associated with investment in these firms and further reduces their access to capital. Given our analytical approach, we would expect that oil and gas companies with level 3 classification are only able to access future capital from one group identified within the financial institution sample.

The second category of oil and gas firms (classified as 2 in Figure 3) is characterized by an acceptance of anthropogenic climate change, limited consideration of climate risk, and a high adoption of the TCFD. We found that 14 oil and gas firms in our dataset commonly referenced anthropogenic climate change as a risk to their business and have begun considering the potential for climate risks. Consideration of subcategory risk varied across this group with firms often disclosing on only one risk subcategory, most frequently regulatory risk. We found that the consistency in data availability and metrics disclosed was higher among firms adopting the TCFD. Firms have begun to quantify and consider the risks associated with the transition to a low-carbon economy, but little attention is given to the opportunities associated with this transition. We found that climate change was primarily framed as a risk to be mitigated by this group. While firms in this group 2 have a high adoption of the TCFD they show no established targets for environmental impact reduction.

The final group assessed (classified as 1 in Figure 3) had the highest number of climate change citations across the three groups and consistently referenced fossil fuels as a factor driving anthropogenic climate change. Across the group, firms connected ESG performance to the firm strategy with major international producers aligning with the Paris Climate Accord and small natural gas firms positioning themselves as the “lowest emission intensity natural gas”. We found that the connection between firm strategy and climate action was supported by an assessment of both the risks and opportunities arising from climate change. Firms in this class seek to minimize exposure to climate risk while investing in initiatives to capitalize on the opportunities associated with the transition to a low-carbon economy. The differentiating feature between class 2 and 1 firms is the establishment of hard targets for reducing environmental impacts. The establishment of environmental targets was connected back to firm strategy and in some firms, executive compensation has been tied to these targets. Focus was on the path to a low-carbon economy and how the transition would impact their business models.

SummaryOverall, we find opportunities for firms to link their sustainability strategy to corporate strategy, to show C-suite commitment to ESG, and to standardize metrics on environmental performance possibly via the use of standard frameworks. With few exceptions, we find a reluctance to admit environmental challenges and shortcomings and to define climate change targets and strategy.

Increasing Investor Interest in ESGInvestors are now concerned with environmental, social and governance (ESG) issues. This interest was accelerated by Bank of England Governor Mark Carney and Michael Bloomberg in 2016. Since then, the highly influential CEO of Blackrock, Larry Fink, has published letters urging organizations to consider ESG factors while highlighting the impact of climate change on financial markets and firm performance [4]. In a review of 19 ESG reports from financial institutions issued in 2018 we find that all declare the importance of ESG. All reports sampled define a dedicated framework for assessing ESG risks within client firms. Firms within the sample acknowledged the role of financial institutions and cited a responsibility to help avoid the consequences of climate change.

Financial institutions play a key role in the oil and gas industry through several channels. They provide financing through direct loans and underwrite liabilities for oil and gas firms. Further, the oil and gas industry is a capital intensive industry requiring significant investment in fixed assets. In their role of providing access to capital for oil and gas firms, financial institutions are uniquely placed to set requirements targeted at influencing firm behavior within client companies. The ability to influence firm behavior is acknowledged throughout the ESG reports reviewed. The sample selected represents the largest public financers of the oil and gas industry with geographic representation in Canada, the United States of America, Europe, the United Kingdom, and Japan (Table 1).

Through participation in investor conferences and conversations with investor analysts, we find that the E in ESG has become a priority. Investors acknowledge the need for better data; the emphasis being on increased consistency and standardization. They are looking for radical transparency from firms aided by technology advances that enable the gathering and manipulation of large amounts of data. Environmental issues, especially climate change, are being factored into investment decisions.

Climate riskIn our dataset, 68% of financial institutions consider climate risk when evaluating oil and gas investments. Climate risk exposes lenders and investors to reputational risk, client default, and limitations to setting internal climate goals. As financial institutions increase their own climate initiatives, client emissions represent a limitation on performance improvements. Wells Fargo has already begun to include these client emissions in GHG disclosures. Due to the wide range of risks and the potential for individual investments to harm the financial institution, most financial institutions reviewed have established board-level oversight for ESG risk. Board oversight of material risks to the firm is considered essential in good governance. Thus, the increased attention to climate risk at the board level highlights the potential materiality of climate related impacts.

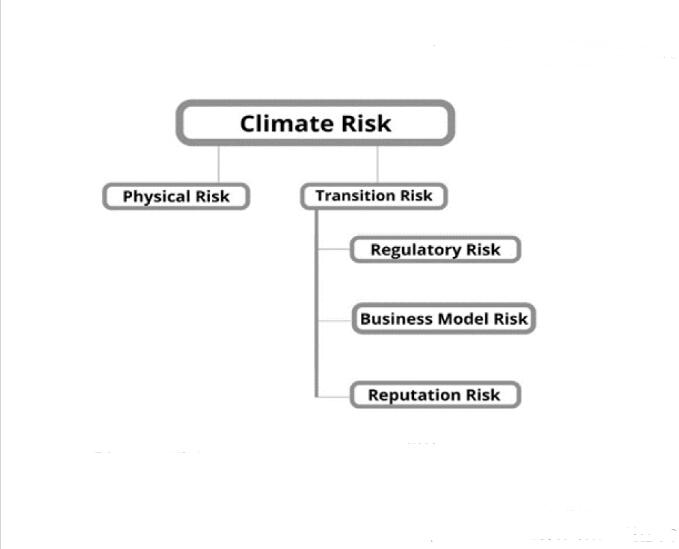

Climate risk is currently broken down into two subcategories: physical risk and transition risk (Figure 4). Specific consideration of subcategory risk is currently used by 53% of the sample. Within the oil and gas sector, the physical risk from climate change includes the potential for impacts to physical assets as a result of changing weather patterns and increased extreme weather events. Many oil and gas assets are located offshore or in regions susceptible to erratic weather, heat, cold, flooding and fires. Investors are concerned with which facilities and operations could be impacted and the strategies in place to plan for or address these impacts. Beyond compromising asset valuation, physical risk increases the potential for financial losses due to the underwriting of oil and gas liability undertaken by financial institutions. Physical risk is considered by the largest proportion of the firms reporting on subcategory risks, but as pressure to take action on climate change has increased financial institutions are increasingly focusing on the broader risks associated with the transition to a low-carbon economy.

Figure 4. Climate risk and subcategory risks.

Figure 4. Climate risk and subcategory risks.

The risks associated with the transition to a low-carbon economy are broken down into three categories: regulatory risk, business model risk, and reputational risk (Figure 4). Regulatory risk is the risk of increased government regulation that restricts or increases the cost of oil and gas development. Common examples of regulatory risk are carbon taxes, stringent methane regulation, and reclamation liability requirements. Regulatory change presents financial risks to oil and gas firms by increasing the cost of production, requiring investments in technology, and restricting access to oil and gas exploration. The potential for reduced profitability through regulatory change increases the risk for financial institutions as currently viable investments may have a compromised ability to repay loans in the future.

Business model risk is primarily concerned with the risk for future loan repayment and business viability. Financial institutions consider a wide range of impacts to the oil and gas business model including environmental liability, fossil fuel demand, and societal pressure. Environmental liability presents the most assessed risk as financial institutions can quantify it. Increasingly the potential for declining global oil demand into the future has been assessed for its impact on firm profitability. While oil demand is projected to continue to increase over the short to medium term, financial institutions are beginning to consider the long-term implications of a low-carbon economy. Tied to the future demand for oil and gas products is the increasing societal pressure to address the source of anthropogenic climate change. We found that financial institutions report facing increased pressure from shareholders and society more broadly to address their role in financing GHG emissions. Therefore, societal pressure presents a risk to both oil and gas firms’ ability to secure regulatory approval directly and financial institutions indirectly through shareholder activism. Assessing the impacts of societal change and future oil demand presents problems in quantifying intangibles. To address the problem in quantification, financial institutions are using scenario analysis to determine the potential for transition risks under a variety of future scenarios. Several firms have begun to develop investment requirements that align with the Paris Climate Accord to ensure their portfolio is compatible with ongoing societal change. For the institutions reviewed the primary concern associated with business model risk is the potential for clients to default on future payments and a compromised financial position. As the world looks to an energy transition, the industry is under threat.

Reputation risk is the risk associated with financial impact due to negative associations with the oil and gas industry. An example of a reputational threat cited by financial institutions is the increasing rise in shareholder resolutions for divestment from oil and gas. Reputation risk has the potential to impact financial institutions across varying dimensions such as firm brand and financial performance. Financial institutions are exposed to brand risk through financial support of oil and gas development, and the tension between the institution’s stated goal of transitioning to a low-carbon economy and continued development of oil and gas reserves is often cited as a reputation risk. Financial institutions have cited negative press coverage due to oil and gas financing as a risk that may drive down firm stock price and limit access to “green” financial opportunities. The financial institutions vary on what is considered a reputational risk with some firms classifying all environmental risk as a reputational risk. Due to the broad nature of reputational risks and the ability for individual investments to impact the overall firm performance, financial institutions are referring all reputational risks to either executive or board level oversight. Having oversight of reputational and financial risks at the executive or board level is important as they are able to consider firm wide risk rather than utilizing a micro-focus on the specific investment under consideration.

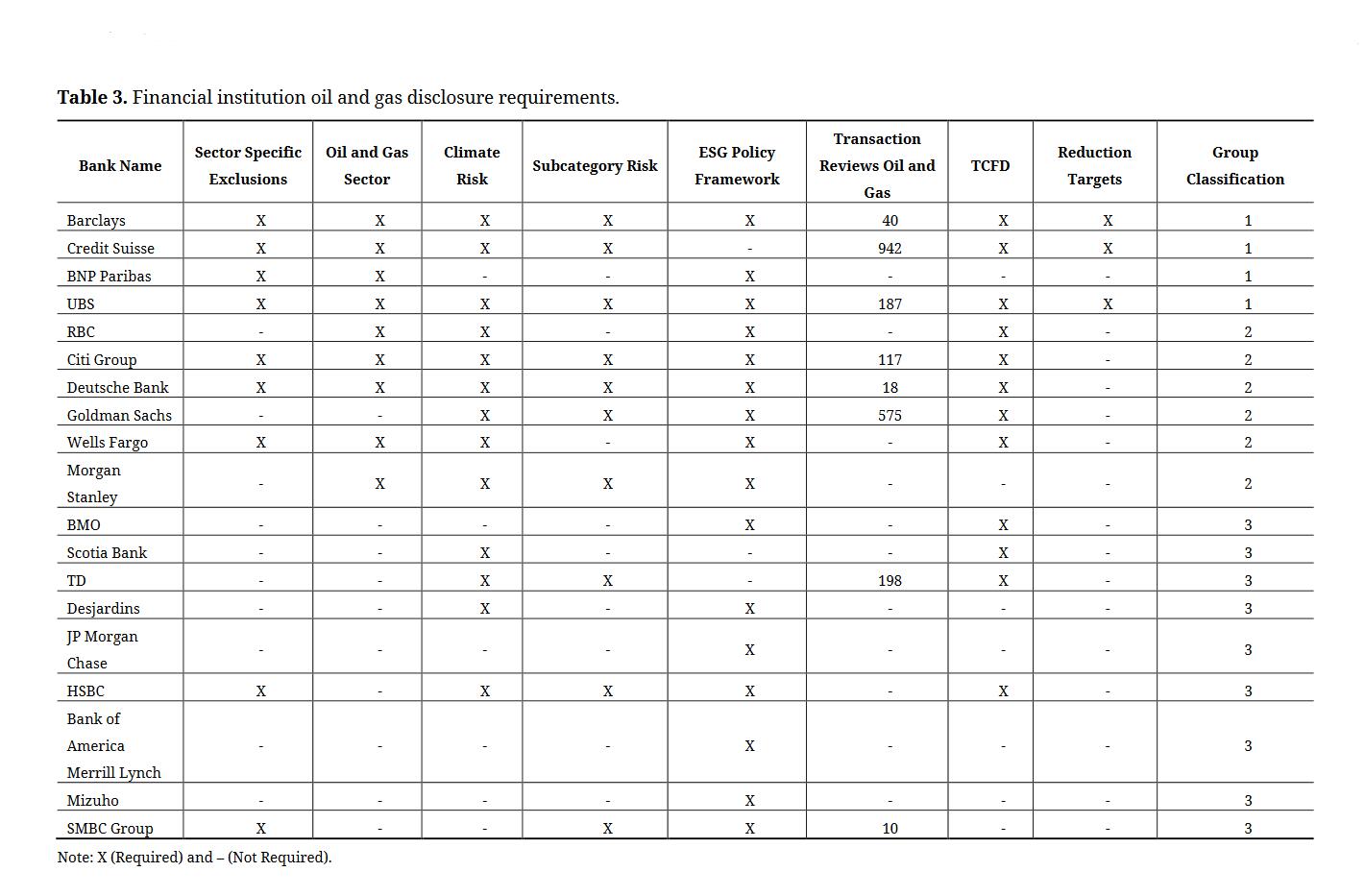

Investor ESG requirements by groupWe categorized financial institutions into three groups based on the stringency of disclosure requirements they place on climate risk when evaluating investment opportunities (Table 3). The first group (classification 1 in Table 3) has the most stringent climate policies of the financial institutions identified. The policies include automatic enhanced due diligence (EDD) for oil and gas investments, consideration of client climate risk, established metrics for disclosure, and sector-based exclusions. Clients must establish environmental goals and show continuous progress. All four firms in this group are European financial institutions. BNP Paribas is included in this group despite lacking hard targets for oil and gas firms as they have stopped all future investment in fossil fuels and begun divestment from current holdings. The establishment of required metrics reflects the greater importance these institutions have placed on exposure to climate risk. Oil and gas firms are required to establish targets for GHG emission reductions and to demonstrate meaningful progress towards these targets. The focus placed on climate risk is transferred to client firms through the requirement for disclosure on subcategory risks. Like other disclosure requirements, the subcategory risk that is required varies by financial institution.

Investor focus on automatic EDD when evaluating oil and gas firms reflects the connection between carbon intense industries and climate change. Both the financial institutions reviewed, and the oil and gas firms have broadly announced support for reducing carbon emissions. Broadly, financial institutions have framed support for a low-carbon transition as helping society address the challenge of climate change. Financial institutions with sector specific requirements look to the companies for use of best in class industry standards, legal and regulatory compliance, and senior manager approval. Industry standards such as ISO 29001 and disclosure frameworks provide assurance that the oil and gas firm is operating in a responsible manner. A heavily regulated industry across jurisdictions (i.e., state/provincial and national/federal) and firm compliance with all applicable laws were cited as decreasing risk exposure. Finally, senior management oversight was framed by financial institutions in this group as providing an overarching view of current firm risk tolerance.

Financial institutions in this group 1 classification (Table 3.) have gone beyond disclosure and performance targets and started to include sector-specific exclusions. Exclusion of the oil and gas sector is still rare among the broader sample analyzed. In the financial institution sample only one firm explicitly excludes the Canadian oil sands and 45% of financial institutions reviewed have specific exclusion criteria for coal and Arctic oil exploration. In contrast, all members of this classification 1 have established sector-based exclusions. Oil and gas firms have increasingly attempted to differentiate the industry from other fossil fuel industries such as coal mining due to the higher impact of coal on GHG emissions and the resulting negative impact on sector reputation. However, we found that financial firms are increasingly including specific forms of oil production with coal as areas that are automatically excluded from investment. Arctic oil exploration and the Canadian oil sands have been focused on as particularly “harmful” forms of oil production. One European financial institution singled out oil sands production using the derogatory moniker “tar sands” to highlight the negative implications associated with this form of fossil fuel development. As oil and gas firms increasingly highlight environmental performance to assure financial institutions of continuous improvement and regulatory compliance, the association between oil and coal may present a risk to future oil and gas projects.

TABLE 3. Financial institution oil and gas disclosure requirements.

TABLE 3. Financial institution oil and gas disclosure requirements.

The second group (classification 2 in Table 3) is characterized by automatic enhanced due diligence (EDD) for the oil and gas sector, minimum disclosure requirements, and requirements for considering the level of climate risk. EDD is a process for increasing the level of scrutiny applied to investments within the oil and gas sector. In the group 2 classification of financial institutions, 83% have specific sector guidelines for investing in oil and gas projects. While the specific procedure for EDD varies between firms, common features across the group were found including review of the investment decision by a dedicated sustainability group. These sustainability groups develop expertise in the assessment of climate risks specific to the sector being considered. The financial institutions reviewed cited the increased expertise as a method of ensuring that climate risk was being appropriately assessed. Four of the six financial institutions in this group are headquartered in America. The requirements for disclosure focused on meeting the jurisdictional regulatory standards of the oil and gas firm. That is, financial institutions in this group have no additional requirements on oil and gas firms beyond those required by law.

The third group (classification 3 in Table 3) was characterized as having no oil and gas review policies, no direct consideration of climate risk, and no sector-based exclusions. This group represents the largest portion of the sample with nine of the 19 financial institutions and the largest concentration of Canadian financial institutions at four of the nine firms. Despite the lack of specific climate risk consideration, most of this group has developed review criteria for ESG issues to be applied for all investments. We found that the amount of capital provided was not a driving factor of the group with only two of the top five oil and gas financers in this category. We found that members of this group have begun to review the process for considering climate risk and have indicated in their ESG reports that more stringent requirements will be implemented in the future. Based on the commitment to increasing focus on climate risk, we expect that this group will progress to group 2 over time.

SummaryWe find that climate risk is paramount in financial institution evaluation of oil and gas investments. This risk assessment considers transition risk which includes regulatory, business model and reputational risk. Investors are concerned with the long-term viability of oil and gas firms given their GHG emissions profiles and their future plans. Consequently, climate risk is tightly tied to overall corporate strategy. Our findings further show that the current disclosure requirements for oil and gas firms have little standardization. Each investment firm reviewed has in-house criteria that are used to determine the viability of an oil and gas investment. These criteria range from stringent requirements imposed by European financial institutions for climate strategy and targets, to technical processes for evaluating oil and gas firms to ensure compliance to strong jurisdictional regulations, to no explicit requirements but indications of moving in that direction.

The growing concern over climate change by financial institutions reflects the role that their industry plays in financing the transition to a low-carbon economy but also its funding of fossil fuel companies. The tension in these often-conflicting goals is evident in changes to investment evaluation and requirements for oil and gas firms. Our analysis of 30 oil and gas firm sustainability reports and 19 financial institution ESG reports results in three key findings. First, Alberta oil and gas firms, while robustly reporting on sustainability, struggle to provide environmental performance data that is consistent across the industry and that adequately conveys climate change responsiveness. Second, financial institutions also vary in their specific environmental requirements for oil and gas investments. In particular, we find that European financial institutions have higher requirements for disclosure and performance especially related to climate change. This has led to the divestment of Alberta oil sands shares by some European investors. Finally, we find that these inconsistencies in reporting and requirements have led to demands for ESG standardization. Our research leads us to conclude that investors will influence standardization towards adoption of the SASB framework and TCFD recommendations.

Sustainability Reporting Inconsistency and Climate Change UnresponsivenessInvestors, as well as the public, require consistent data across companies to make fair comparisons in evaluating relative performance. Inconsistency in metrics, units, and time present several challenges in making direct comparisons across the sample of sustainability reports. We found that the metrics reported varied with some firms failing to report on GHGs entirely. Even where similar metrics were provided the associated unit of measure and time scale (e.g., two vs five years) differed. The greatest inconsistency in data representation was regarding climate risk. Firms that fared better on climate risk identified their exposure and showed investments and plans for transitioning to a low-carbon economy. Further, clear C-suite commitment was indicated. Large MNCs were most effective at defining their climate change strategy and showing its connection to corporate strategy.

Our data suggests that an evolution in disclosure is occurring. Sustainability reports are now important mechanisms for communicating to investors a commitment to ESG performance. Larger integrated oil companies are taking the lead. This may be due to their established relationships with large institutional investors. The most advanced of the MNCs are global companies with headquarters in Europe. Our data also indicates that European investors are leaders in requiring climate change responsiveness. Alberta oil and gas firms can build on the actions of these companies and potentially leapfrog in disclosure approaches as standards are being set.

Investor Requirements for Strategy and IntentESG has emerged as a key concern of investors. The E or environment is of particular concern when evaluating firms in environmentally sensitive industries. And within the E climate change risk takes center stage. There was variance in the stated climate change requirements of the 19 investor ESG reports that we analyzed. This presents a challenge for oil and gas companies that attempt to expand disclosure and respond to investor demands.

Investors have moved beyond considering financial risk tied to climate risk in the form of physical effects and regulatory risk [48] to transition risk which expands to include business model risk and reputational risk. This is important because these factors are endogenous to the firm and within its control, in contrast to exogenous natural disasters and imposed regulations. Investors thus are concerned with corporate strategies that address transition risk in executable ways. At a minimum, consistent, standardized reporting on GHGs is required and there is a push to requiring articulation of a climate change and transition strategy that includes targets and progress. Some investors are implementing specific exclusions for coal and Artic exploration and in some cases oil sands.

Climate change will become a bigger issue in the future, and we expect investor requirements to only become more stringent. Alberta oil and gas firms must consider this eventuality as a threat and respond effectively through radical transparency and implementation of climate change strategy and risk mitigation.

Towards StandardizationOur key finding is that there is a lack of consistency in BOTH investor requirements and oil and gas firm reporting. This finding aligns with supporting data from investors and companies that expressed confusion and frustration. Investors are frustrated with inconsistent reported data that makes comparative analysis difficult. Oil and gas firm representatives are confused as to what exactly should be reported. The fractured nature of data requirements places additional pressure on oil and gas firms to prepare disclosures that meet the requirements of a diverse group of institutions. There is a need for standardization. And yet, customization applied by financial institutions has merit and each oil and gas firm is unique in its operations and practices. It is unclear whether ESG and especially environmental reporting can reach the level of standardization that accounting principles have created. Even so, the current drive among financial institutions to adopt the TCFD recommendations and SASB frameworks may decrease the variability across firms and allow for more uniform disclosure by oil and gas firms. By increasing the uniformity of requirements and disclosures, financial institutions will be able to compare oil and gas ESG performance across the industry.

The TCFD and SASB frameworks encourage disclosure of financially material environmental risks across defined categories. Firms already adopting these frameworks show greater consistency in data availability and metrics. We do not see firm size as a barrier to adoption given that two small cap firms in our data set are using the SASB framework.

Oil and gas firms that do not meet the requirements of over half of the financial institutions in our sample face the possibility of restricted access to capital or even divestment. As the financial industry, via BlackRock’s stipulation, moves to requiring application of the TCFD and SASB frameworks, Alberta oil and gas companies must follow the lead of international companies that develop scenario planning and adhere to TCFD recommendations [1].

We see opportunity for firms to clearly define a sustainability or climate change strategy and to link this to overall corporate strategy. Large MNCs have taken this approach and outline their plans for addressing climate change risk and business model risk due to the energy transition. Alberta centric and smaller firms can do more to report GHG emissions and to define goals. The lack of acknowledgement of climate change and its impact to the business model by most of the Alberta firms calls into question intent.

ContributionsWe contribute to the sustainability reporting and ESG literature. Our overarching contribution is to show how financial institutions, or investors more broadly, have significantly influenced firm level disclosure through increasing requirements for climate change action. This expands the literature on sustainability reporting and ESG disclosure by highlighting the importance of investors as stakeholders and by demonstrating their ability to affect, in addition to being affected via investment impact, firm environmental performance. Additional contributions are to show, through empirical evidence, the problem of inconsistencies not only in oil and gas corporate sustainability reporting but also in financial institution criteria for evaluating those firms as potential investments. Extant literature addresses quality and consistency issues in sustainability reporting but does not consider similar challenges with investor requirements and the potential for standardization that addresses both shortcomings. In this way, we connect the established literature on sustainability reporting with the growing ESG conversation.

Our findings on disclosure inconsistency support the extant literature on sustainability reporting with one exception. We find evidence of smaller sized firms adopting SASB standards, establishing sustainability strategies, and reporting consistent and fulsome data. The lag in larger firms moving towards TCFD as a standard may be explained by the path dependency and inertia associated with reporting tied to other frameworks like GRI. We expect investor pressure to expedite the shift to an industry standard.

We further contribute to the ESG literature by highlighting the “E” and the tension financial institutions have in addressing climate change while evaluating investments in oil and gas firms. While the G in ESG is considered critical in the literature, we find that the E becomes paramount when considering certain sectors and companies such as oil and gas. Firms and investors are being pulled to radical transparency on environment given the grand challenge of climate change and the response by governments and society.

Managerial ImplicationsOur findings have important implications for Alberta oil and gas firms. We show that oil and gas firms must move beyond data reporting, although this remains critical, to demonstrate strategic consideration and intent regarding climate change risk. This means addressing transition risk and showing how the company will survive and thrive through a global energy transition to a low carbon economy. The connection between environmental performance and overall corporate strategy must be clearly defined. CEOs and executives play a key role in communicating this commitment. Firms that ignore the importance of strategic intent on climate change exclude themselves from access to capital.

Investor ESG requirements have played an important role in augmenting the importance of sustainability reporting and consideration of climate risk for all firms. This is especially true for environmentally sensitive sectors like oil and gas. Former approaches to disclosure are no longer sufficient. Investors, governments, and society are demanding a transparent and substantive response to climate change risk. By failing to consider the risks and opportunities associated with a transition to a low-carbon economy, firms are failing to address a fundamental shift in the energy industry.

Our findings are inline with the broader literature on ESG disclosure highlighting quality and comparability problems. Cardoni et al., [5] noted that the comparability issues in ESG disclosure present problems for researchers if not addressed. This finding is consistent with both our research presented here and the broader literature [5]. However, when assessing the level of disclosure in relation to one stakeholder group, the lack of comparability is an indication of the differing responses to stakeholder pressure. Therefore, disclosure comparability is not a direct problem in the present study, rather an area of investigation.

While the sample analyzed here is limited to oil and gas firms with substantial operations or headquarters in a singular region [49], a large proportion of both smaller-cap and larger-cap firms analyzed also have operations in other regions globally. Several of the larger-cap firms analyzed are also headquartered outside of the region. Accordingly, while it is possible the findings may not be fully representative of the global oil and gas industry, region specific biases (such as common disclosure or environmental regulatory regimes) or region specific ESG challenges (such as degree of water scarcity or human rights violation risk) are not expected to have substantially influenced the results. Additionally, while the present study uses a relatively small sample of oil and gas firms (30 firms), a wide range of firm sizes is represented (market capitalization between $127 million and $327.2 billion USD) and total market capitalization of $1.3 trillion USD is included. This provides a representative cross-section of the oil and gas industry while ensuring a reasonable scope for the labour-intensive content analysis process, but may not reflect the full range of variability between firms.

Similar future efforts may achieve greater global generalizability from inclusion of a larger number of firms, and inclusion of firms with both corporate headquarters and primary operations in a more diverse subset of regions. Further, future research could benefit from a longitudinal analysis of financial institution industry disclosure requirements and resulting changes in oil and gas firm disclosure. Additionally, while the financial institutions in our sample are both invested in global oil and gas and the Alberta oil sands specifically, future research could attempt to link financial institution investments with individual firms.

CVdB and JD designed the study. JD and MM collected, coded, and analyzed the data. JD and CVdB wrote the paper with input and editing from MM.

The authors declare that there is no conflict of interest.

This research was funded by Imperial through Mount Royal University’s Institute for Environmental Sustainability.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

Dye J, McKinnon M, Van der Byl C. Green Gaps: Firm ESG Disclosure and Financial Institutions’ Reporting Requirements. J Sustain Res. 2021;3(1):e210006. https://doi.org/10.20900/jsr20210006

Copyright © 2021 Hapres Co., Ltd. Privacy Policy | Terms and Conditions