Location: Home >> Detail

J Sustain Res. 2025;7(1):e250010. https://doi.org/10.20900/jsr20250010

,

Péter Molnár 1 ,

Árpád Tóth 2

,

Péter Molnár 1 ,

Árpád Tóth 2

1 Doctoral School of Regional and Economic Sciences, Széchenyi István University, Győr 9026, Hungary

2 Statistics, Finance and Controlling Department, Széchenyi István University, Győr 9026, Hungary

* Correspondence: Bence Lukács.

Background: This research examines the efficiency of ESG reporting in corporate contributions toward achieving the SDGs, relative to the literature gaps and sectoral differences in reporting practices. It also highlights that full ESG disclosure is invariably instrumental in ensuring corporate transparency and accountability.

Methods: The study used the GRI framework to analyze SDG compliance in sustainability reports from companies in the technology, automotive, energy, and health sectors.

Results: Key findings include significant variations in SDG compliance across industries: the automotive sector demonstrated the highest compliance at 85%, while the technology sector showed the lowest at 49%. The study also found a notable difference between reported and substantiated SDGs, indicating that many companies engage in ‘rainbow washing’ or ‘cherry-picking’ SDGs to fit their agendas without fully integrating them into their strategies. The research concludes that although the GRI framework provide.

Conclusions: The study urges the combination of other standards, such as ESRS and SASB, together with more intense regulatory frameworks and industry-specific guidelines to increase comparability and the credibility of the reports on sustainability.

ESG, environmental, social, governance; SDG, sustainability development goals; GRI, global reporting initiative; SASB, sustainability accounting standards board; ESRS, European sustainability reporting standards; TBL, triple-bottom line; UN, United Nations; CSRD, corporate sustainability reporting direcitve; IIRC, international integrated reporting council; KPI, key performance indicatior; SRS, SDG Reporting Score; TCFD, task force on climate-related financial disclosures; KLD, Kinder, Lydenberg, Domini

The United Nations established the Sustainable Development Goals in 2015 as an international framework aimed at tackling interconnected social, economic, and environmental issues. Realizing these 17 goals requires a joint effort of governments, businesses, and communities in a view of sustainable and fair development. One of the important ways this can occur is through corporate transparency and accountable reporting systems that link organizational performance with the goals of the SDGs. ESG reporting has become a key tool in assessing the sustainability initiatives of corporations. Structured methodologies like GRI, SASB, and ESRS provide structured frameworks. The GRI framework is one of the most implemented tools due to its focus on the triple bottom line: economic, social, and environmental dimensions. It is mainly used to align practices in businesses with the SDGs. However, the voluntary nature inherent in most ESG frameworks has resulted in diversities, selective disclosure (“cherry-picking”), and a perfunctory integration of SDGs within corporate strategies (“rainbow washing”). The literature brings forth both the promise and limitations of sustainability reporting as it stands today. For instance, while GRI indicators support structured SDG reporting, numerous studies have shown significant variation across industries and regions. Some sectors like automotive and healthcare show better compliance, while technology and energy often trail. This raises concerns about the comparability, credibility, and completeness of corporate sustainability disclosures. To fill these gaps, this research evaluates corporate SDG compliance, using the GRI framework across key industries: technology, automotive, energy, and healthcare. With quantification of SDG contributions and categorization into ESG pillars, the research tries to give an in-depth and comparative assessment of sectoral performance. It flags disparities in reporting but also calls for harmonized frameworks and regulatory interventions that could make sustainability reporting more credible.

SDGs and ESG ReportingReaching and contributing to the SDGs are increasingly important for companies all around the world. The GRI indicators are one recommended methodology to measure progress toward the SDGs, enabling organizations to report their contribution in a more structured and quantitative way. According to Calabrese et al. [1] and Aguado-Correa et al. [2], the GRI guidelines and indicators make it easier for companies to report on SDGs. Another advantage of the GRI framework is the embedding of the ‘double bottom line’ principle-meaning impacts on both companies and society and the environment. Whereas the CSRD and EU Taxonomy in the European Union provide some sort of guidance and obligation for companies, the Securities and Exchange Commission in the United States allows freedom for companies in general to decide on the content of reporting. Küçükgül et al. [3] give emphasis to the call for harmonized reporting frameworks. They, in fact, call for a single framework, which would be instrumental in propounding the attainments of the SDGs through efficient reporting. Indeed, both the IIRC and GRI endorse this approach based on promoting organizational transparency and accountability. Understanding the various systems and methodologies concerning sustainability reporting has a significant relevance for the companies regarding the correctness in communicating their sustainability performances. In turn, the GRI framework is based on the TBL principle, which was an even more integrated economic, social, and environmental dimensions of disclosure. From this perspective, companies may show a complete view of their performance, which consists not only of environmental impacts but also of social responsibilities and financial results.

Selective ReportingHowever, a literature review by [4] found that while statements related to SDG were common, reports with backup through tangible indicators were few and far between. The ‘rainbow washing’ phenomenon suggests that companies usually do not integrate the SDGs into their strategies, while merely using SDG logos for awareness. ‘Cherry-picking’—where companies select only the SDGs relevant to themselves—is also common. Energy companies often fail to provide adequate reporting on their efforts to contribute to the SDGs [5]. Supporting this, another research shows that companies disclosing high levels of environmental GRI information stand higher in ranking on the environmental SDGs [6]. The GRI reporting of European car manufacturers is associated with the SDGs; thus, all 17 SDGs were covered with relevant KPIs, according to [7]. Furthermore, the SRS index based on SDG Compass can measure the level at which companies report against expected indicators [8]. In the Refinitiv ESG database 40 SDG goals could be identified as measurable by ESG score [9]. They comment that SDGs are more interpretable at the government level compared to the company level. As indicated by Jonsdottir et al. (2021), While the adoption of the ESG framework may have some financial returns for a firm, SDGs are more about achieving a sustainable future, and hence this may pose a challenge in trying to integrate them into ESG [10]. In another study, ERI indicator was developed to measure the relevance of the SDGs on the 30 generic ESG items defined by SASB [11]. The ERI indicator was further elaborated by [12], to explore SDGs relevant for health. When examining the ESG databases, no relationship was found between ESG scores and SDG scores [13].

Transparency in ESGAdditionally, according to [14], in many cases, the relationship between ESG and financial performance is obscure. In addition, ESG monitoring is possible with an Audit 4.0 basis, but it needs supplementary studies to make a real practice. ESG reporting practices are also considerably influenced by industry-specific factors because industries face different degrees of ESG regulatory pressures. For example, high carbon industries such as energy and manufacturing would have more detailed environmental metrics, while service-oriented sectors would highlight their social responsibility and governance issues [15]. Alkaraan et al. [16] find that effective governance mechanisms, such as ESG oversight and board expertise, in concert with Industry 4.0 technologies, are associated with improved quality, transparency, and reliability of ESG reporting. Firms’ technological adoption and dynamic capabilities, therefore, enable the proper tracking and integration of ESG metrics, hence guaranteeing comprehensive and decision-relevant disclosures that are concordant with sustainability objectives. Furthermore Alkaraan et al. [17] identifies that green servitisation innovation-facilitated Industry 4.0 technologies and corporate governance mechanisms significantly enhance ESG performance by improving the sustainability practices of the whole value chain. Industry 4.0 enables companies to incorporate green innovation strategies into their green sustainable supply chain management (GSSCM), while strong governance structures, in terms of board oversight, CSR committees, and gender diversity, ensure accountability and alignment toward ESG goals. This nexus of digitalization and governance bolsters the capabilities of companies in mitigating environmental impacts, improving social outcomes, and increasing transparency in ESG reporting.

Disagreement in ESG RatingsVarious ratings for ESG have been carried out because there were several methods and routines, discrepancies in data quality, subjectivity in evaluation, sectors, and updates of assessment frameworks. These differences are expressed in the choices and weighting of assessment criteria and in the various applications of rating systems. Such huge differences may be accountable to significant inconsistency in data and subjectivity in ESG ratings. Indeed, inconsistency in reporting ESG data poses a huge challenge to analysis because the variation in metrics makes the comparison of companies difficult and the selection of the best performing companies is at challenge [18]. This problem is further compounded by the fact that data is not generally available, and the benchmarks against which comparisons are needed may be hard to identify. ESG data providers define benchmarks differently, which influences the interpretation of ESG scores and sometimes leads to discrepancies [19]. Minimum standards of international ESG index funds may be another explanation for significant differences in the composition of funds based on the various ESG scores of companies. An example can be seen in the ESG score of Yahoo Inc., which has varied quite dramatically over the years, especially in the social dimension. This once again puts into light the relevance of considering ESG levels and risk. For instance, ASSET4 and Bloomberg might indicate a higher risk within the social dimension, while KLD might indicate a higher risk in corporate governance. Besides that, another significant cause of variance within ESG ratings is the dissimilar methodologies different rating agencies are adopting. The agencies may attach different importance regarding ESG factors, sources, and weighting, therefore leading to inconsistencies in the results for an entity [20]. Standardization will enhance consistency in the assessment and reporting of ESG factors and thus enable more valid comparisons concerning the sustainability performance of companies. Discrepancies in the ratings also could be reduced by standardized ESG reporting frameworks, developed by SASB or GRI, for example, and collaboration across sectors in developing common standards [21].

Aims and ContributionThis paper will attempt to provide a measurable assessment of SDG adherence via the GRI framework, as well as some of the industry-specific challenges. This research contributes to the continuing debate on ESG reporting, bringing a critique of the current frameworks but also a pathway toward improvement. By casting light on sectoral differences, this supports policymakers, businesses, and all other stakeholders in fostering genuine corporate engagement in global sustainability goals.

The methodology followed in the study represents a systematic approach toward corporate SDG compliance based on the GRI framework. The analysis was performed in three main steps: first, identification of GRI indicators linked with the targets of the SDGs within the corporate sustainability reports, second, calculation of the SDG compliance ratio and divergence across sectors, and third, classification of SDG contributions into the ESG pillars for assessment of sectoral performance. This would ensure the comprehensiveness in assessment of the reported and substantiated contributions to SDGs while highlighting sector-specific trends and discrepancies.

In the first part of the primary research, an SDG compliance analysis was carried out. For the analysis, the GRI [22] document “Linking the SDGs and the GRI standards” was used. The document includes all GRI items that can be linked to the SDGs with the approvement of GRI and the UN. This makes it possible to determine which SDG targets can be linked to a given GRI item and how many GRI items can be linked to a given SDG. For the practical application of the GRI document, it was necessary to review ESG reports of real companies, including the so-called “GRI content index” subchapter subdocument [22]. By listing the reported GRI items for a given company, it was possible to specify the percentage of the reported GRI items that cover the items in GRI that are linked to the SDGs [22]. The latter part of the methodology is shown in Figure 1.

Figure 1. Applied methodology.

Figure 1. Applied methodology.

A detailed description of the methodology is shown in Figure 2.

Figure 2. Applied methodology detailed version.

Figure 2. Applied methodology detailed version.

The second step involved calculating the level of “SDG compliance based on GRI; reported SDG compliance; average compliance ratio per 1 SDG; SDG divergence”. SDG divergence underlines the difference between reported and supported SDGs. A positive divergence would mean that the companies align with more SDGs than they report, suggesting underreporting or missed communication opportunities. A negative or zero divergence would indicate potential issues of overreporting (rainbow washing) or consistent alignment, respectively, and calls for increased transparency and regulatory oversight in sustainability reporting.

Formulas:

The study analyses sustainability reports from the one of the most significant companies (Table 1) in the technology, automotive, energy and healthcare industries. The industries were selected due to their major economic impact and critical contribution to achieving the SDGs. Collectively, these sectors represent one of the largest contributors to global GDP [23]. Hence, given the significant ESG impacts of these sectors, they are critical for assessing the corporate contribution to the SDGs and hence present a pathway for further improvements and better alignment with global sustainability objectives.

Table 1. Names of companies examined by industry.

Table 1. Names of companies examined by industry.

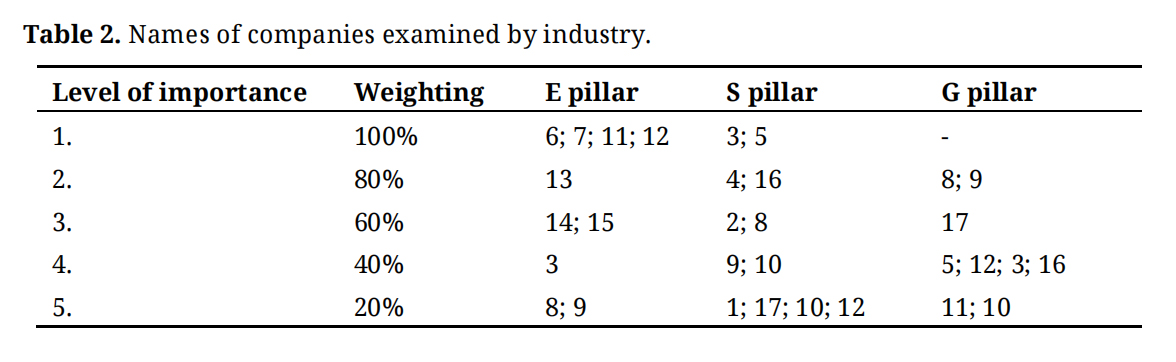

In the third step of the research, based on the study by Lukács and Rickards [24], the SDGs supported by company reports were classified into ESG pillars (Table 2). The classification provided an indication of which pillar the company contributed to, with the percentage of SDGs compliance scored as a point on a scale of 0–100. Lukács and Rickards [24] also determined the classification of SDGs into ESG pillars based on the GRI reporting items, so the present methodology is based on the same principles as the methodology used as a starting point. Furthermore, a prioritization of the SDGs in terms of ESG has been defined. The contribution levels were weighted according to this order.

Table 2. Names of companies examined by industry.

Table 2. Names of companies examined by industry.

In this session, the results of the first methodology will be presented and analyzed. Table 3 shows a summary of the data of the surveyed companies by industry. The highest GRI scores were achieved by the automotive companies surveyed, while the lowest GRI scores were achieved by the technology companies surveyed. The highest number of SDGs was achieved by the surveyed healthcare companies, while the highest number of SDGs supported was achieved by the surveyed automotive companies. The difference between reported and substantiated SDGs gives an indication of how many fewer SDGs the surveyed companies reported than they contributed according to their GRI reporting.

Table 3. Results by sector.

Table 3. Results by sector.

Table 4 summarizes the descriptive statistics of the GRI items reported by the surveyed companies by industry. The data shows that on average, the automotive companies surveyed reported the most GRI items, while the technology companies surveyed reported the least. The automotive companies surveyed also had the highest median value, while the automotive companies surveyed also had the lowest variance in the number of GRI items reported. This suggests that the automotive companies surveyed consistently use GRI items and the companies surveyed actively report sustainability performance using the GRI methodology. The highest GRI item reporting was nevertheless found in one company surveyed in the healthcare sector, as was the lowest number of GRI item reports.

Table 4. Descriptive statistics of reported GRI items by sector.

Table 4. Descriptive statistics of reported GRI items by sector.

Based on the number of GRI items reported, the SDG compliance of the surveyed companies by industry is illustrated in Table 5. The highest average SDG compliance was for surveyed companies in the automotive industry with 85%, while the lowest was for surveyed companies in the technology industry with 49%, a difference of 36%. The average SDG compliance of companies surveyed in the energy industry was like that of companies surveyed in the healthcare industry with SDG compliance ranging from 70% to 71%. Across the board, the companies surveyed in the automotive industry performed the best, while the highest SDG compliance score was achieved by a company surveyed in the healthcare industry.

Table 5. Descriptive statistics of SDG compliance based on GRI.

Table 5. Descriptive statistics of SDG compliance based on GRI.

In Table 6, it was examined whether there is a significant difference in the number of GRI items reported by the companies surveyed. The chi-squared analysis shows that there is a significant difference at the 0.01 level for all, but the companies surveyed in the energy and health and safety industries. The chi-square test results indicate significant differences in the reporting of GRI items among industries, except that energy and health industries reported statistically similar results. In other words, industries like the automotive and technology industries showed distinctively different reporting behaviors, and the automotive firms generally reported the highest number of GRI items. Such practices surely signal an increasing need for standardization across industries to advance comparability and transparency in sustainability reporting. Furthermore, the results indicate that there is a significant variation in GRI reporting performance between the companies studied at the industry level.

Table 6. Chi-squared analysis of reported amount of GRI items by sector.

Table 6. Chi-squared analysis of reported amount of GRI items by sector.

The SDGs reported by the surveyed companies were found not to cover the GRI-based SDG compliance of the surveyed companies, as illustrated in Table 7. When reviewing the minimum values, for some of the companies surveyed there is less than 100% compliance, meaning that in some cases the number of SDGs reported was higher than the number of SDGs that could be supported by GRI.

Table 7. Descriptive statistics of an average SDG compliance for one SDG.

Table 7. Descriptive statistics of an average SDG compliance for one SDG.

Results of the second methodology of the primary research and their analysis in this section are presented in this section. The descriptive statistics of the calculated ESG compliance based on the contribution to the SDGs are shown in Table 8. For each of the pillars, the automotive companies studied performed the best on average. For the social pillar, the highest contribution score was achieved by a company surveyed belonging to the health industry. In the environmental pillar, at least one company in all other industries except energy scored the same highest. As in the social pillar, the highest contribution score for corporate governance was achieved by a company in the health sector.

Table 8. Descriptive statistics of calculated ESG ratings based on SDG contribution.

Table 8. Descriptive statistics of calculated ESG ratings based on SDG contribution.

Table 9 summarizes the average ESG scores of the surveyed companies by industry. The ESG scores of Refinitiv [25] and S&P Global [26] ESG score providers and the ESG scores obtained because of the primary research are summarized. For the environmental pillar, the healthcare industry received the highest average ESG score from Refinitiv and S&P Global, respectively. Based on the proprietary results, the automotive industry received the highest score in the environmental pillar. Also in the social pillar, the healthcare industry scored the highest average ESG score from both Refinitiv and S&P Global. For own results, the automotive industry also received the highest average ESG score in the social pillar. In the corporate governance pillar, the healthcare industry received the highest average ESG score from both Refinitiv and S&P Global, while own results showed the automotive industry as the best performer.

Table 9. Average calculated ESG ratings by sector.

Table 9. Average calculated ESG ratings by sector.

As a statistical test of the ESG score of service providers and the present ESG results, a chi-square test was performed (Table 10). The chi-square test shows a statistically significant difference between the different score provider results for the technology companies under study. The difference between the scores cannot be due to scaling bias, as all ESG scores considered have the same 0–100 scale interpretable (worst to best). Previous studies confirm that ESG scores differ across service providers [27].

Table 10. ESG ratings divergence between Technology companies with chi-squared analysis.

Table 10. ESG ratings divergence between Technology companies with chi-squared analysis.

For the automotive firms examined (Table 11), there is a small difference in significance between S&P Global’s Refinitiv and Refinitiv and the present results.

Table 11. ESG ratings divergence between Automotive companies with chi-squared analysis.

Table 11. ESG ratings divergence between Automotive companies with chi-squared analysis.

For the energy companies surveyed (Table 12), there is only a significant difference between the ESG score of S&P Global and the ESG score of this study.

Table 12. ESG ratings divergence between Energy companies with chi-squared analysis.

Table 12. ESG ratings divergence between Energy companies with chi-squared analysis.

There is a significant difference between the results of S&P Global and the present study, and between the results of the present study and the Refinitiv values for the health care companies studied (Table 13).

Table 13. ESG ratings divergence between Health companies with chi-squared analysis.

Table 13. ESG ratings divergence between Health companies with chi-squared analysis.

A review of the research findings on the SDGs’ compliance by organizations using the GRI framework provides evidence of great variance among industries. The automotive industry demonstrated the highest compliance, whereas the technology sector reported the lowest. This indicates discrepancies in the practice of sustainability reporting and further supports prior evidence where studies showed variability in industry reporting quality and comprehensiveness for sustainability information disclosure.

One important observation to be made is some form of rainbow washing practice where companies use SDG logos without embedding the goals in their strategies. This, together with ‘cherry-picking’ of SDGs that best fit specific corporate agendas, will essentially point to a superficial commitment to sustainability. To respond to “rainbow washing” and “cherry-picking”, companies need to go beyond superficial SDG alignment, including obligatory verification mechanisms of SDG claims through, for example, third-party audits or independent certifications. Regulatory bodies should insist on standardized ESG reporting frameworks like GRI, ESRS, or SASB so that the claimed SDG contributions are substantiated by the real indicators. A holistic set of guidelines and penalty systems that are industry-wide may help create real accountability, potentially reducing the credibility gap between sustainability disclosures. These findings are in line with the work of [5], where it was established that energy companies, in most cases, do not provide sufficient information about their activities in support of attaining the SDGs.

The study also strongly puts forward the need to have a more comprehensive and inclusive approach when it comes to the monitoring of compliance with SDGs. The research at hand relies on the GRI framework and therefore restricts monitoring and assessment only to those companies that apply this specific reporting standard. Other approaches, such as the ESRS and SASB, can illustrate more broadly and accurately their contributions to the SDGs. A single framework can help improve reporting toward the SDGs according to [3]. The inconsistency in ESG reporting practices in UK firms can increase investor uncertainty, leading to a higher cost of capital, contrary to expectations [28]. With the harmonization of reporting frameworks, such as GRI, SASB, and TCFD, could improve transparency, comparability, and reliability, reducing perceived risks and lowering capital costs.

Furthermore, it follows from this fact that some industries, such as automotive and healthcare, have satisfactory performance in certain ESG pillars, while at the same time there are industries with unexpectedly low results. With such uneven scoring in the industries, it can be concluded that some industries require industry-specific guidance and assistance to raise overall levels of adherence to more satisfactory levels.

Managerial ImplicationsThe findings of the study indicate critical managerial implications for improving sustainability reporting and SDG alignment. The results indicate significant gaps between reported and substantiated SDGs, pointing to potential “rainbow washing” and “cherry-picking”. Such gaps could be minimized by enhanced governance mechanisms and the adoption of sector-specific guidelines that ensure transparency and credibility. By adopting standardized frameworks such as GRI, ESRS, or SASB, together with real-time monitoring technologies, managers will be able to enhance ESG performance, improve investor trust, and contribute more effectively to global sustainability goals.

This research points out the critical importance of ESG reporting in harmonizing corporate activities with sustainability objectives within the framework of the GRI and its relationship with SDGs. The outcomes across sectors show differences as superior compliance was demonstrated by automotive while deficiencies are noticed within the technology sector, hence inconsistent integration and reporting of the sustainability initiatives. Notably, it points out challenges in “rainbow washing” and “cherry-picking” of SDGs, which signals the requirement for better regulatory oversight and industry-specific guidelines for the assurance of transparency and credibility. This research is consistent with studies by [3] and [5], putting an emphasis on the harmonization of reporting frameworks like GRI, ESRS, and SASB to increase comparability and deal with inconsistencies across industries.

The most important finding of this study is to provide empirical evidence on the requirement for a better-integrated and comprehensive reporting framework that reduces fragmented sustainability disclosures. This can be further enhanced by integrating Industry 4.0 technologies with robust governance mechanisms in reporting quality, as noted by [16], where technology adoption facilitates real-time monitoring and governance assures congruence with the objectives of sustainability.

There are, however, some limitations of this study. The central focus of GRI-based reporting research may, in fact, limit the inclusion of other framework perspectives, including those of TCFD or SASB. Future research should, therefore, consider integrated reporting practices that use multiple standards with a view to offer a holistic assessment of SDG compliance and ESG performance. Furthermore, research analyzing the effectiveness of regulatory initiatives, such as the EU Corporate Sustainability Reporting Directive [29], in increasing consistency in reporting across industries would be most enlightening. Such challenges must be overcome to make ESG reporting credible, transparent, and actionable for driving the global sustainability agenda forward. A similar study using other ESG reporting frameworks has not yet been carried out and therefore the results are not yet replicable to other studies. As a future research direction, extending this is considered a relevant and beneficial goal.

The dataset of the study is available from the authors upon reasonable request.

Conceptualization, LB; Methodology, LB; Software, LB; Validation, MP, TÁ; Formal Analysis, LB; Investigation, LB; Resources, LB; Data Curation, LB; Writing—Original Draft Preparation, LB; Writing—Review & Editing, LB and MP; Visualization, LB; Supervision, TÁ; Project Administration, LB; Funding Acquisition, LB.

The authors declare that they have no conflicts of interest.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

Lukács B, Molnár P, Tóth Á. Measuring Corporate Compliance with the SDGs Based on the GRI’s ESG Reporting Methodology. J Sustain Res. 2025;7(1):e250010. https://doi.org/10.20900/jsr20250010

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions