Location: Home >> Detail

J Sustain Res. 2025;7(4):e250065. https://doi.org/10.20900/jsr20250065

,

Ghodratollah Haidarinezhad 2

,

Ghodratollah Haidarinezhad 2

1 Crews School of Accountancy, Fogelman College of Business and Economics, The University of Memphis, Memphis, TN 38152, USA

2 Department of Accounting, Payame Noor University, Tehran PO BOX 19395-3697, Iran

* Correspondence: Zabihollah Rezaee

Purpose: This study investigates the relationship between gender diversity in audit committees and the financial performance of firms in Iran, a developing economy characterized by a weak corporate governance structure and notable gender disparities.

Design/Methodology/Approach: Utilizing a dataset of 1058 firm-year observations from Tehran Stock Exchange (TSE)-listed firms between 2013 and 2019, this study examines the impact of female representation in audit committees on both financial and market performance.

Findings: The results reveal that the presence of at least one woman on an audit committee positively influences firms’ financial and market performance. These findings remain robust after addressing potential endogeneity concerns.

Practical Implications: The study offers valuable insights for policymakers and regulators, highlighting the role of gender diversity in strengthening corporate governance and enhancing financial performance.

Originality/Value: By examining the effects of gender diversity in audit committees within a developing-country context, this study contributes to the literature by shedding light on an under-researched area.

In recent decades, gender diversity on corporate boards and audit committees has become a central topic in the corporate governance literature. While numerous studies suggest that women’s participation can improve firm performance by reducing discrimination, enhancing decision-making, and increasing legitimacy, empirical findings remain mixed and inconclusive across countries. Some research documents a positive effect, while others find neutral or even negative outcomes. Globally, women still hold only 23.3% of board seats, according to the 2024 Deloitte global survey, indicating that less than one-fourth of top leadership positions are occupied by women despite continuous progress [1]. Building on this global evidence, prior research has extensively examined the impact of women’s presence on corporate boards over the past decade [2–5]. Board gender diversity is believed to influence firm performance through two primary channels: reducing gender discrimination and leveraging diversity advantages [6], as well as ensuring compliance with mandatory gender equality regulations [7,8]. Despite increasing attention to this issue, prior studies present mixed and often inconclusive findings regarding its financial implications. While some research highlights a positive relationship between female board representation and firm performance [9–13], others suggest no significant effect [14–16], and some even report a negative association with financial and market performance [17–19]. Most of these studies have been conducted in developed economies such as the United States [20–22] and Europe [5,11,23], with limited research in emerging markets like China [3] and Nigeria [24].While prior studies have explored gender diversity and firm performance across different economic contexts, this study addresses a critical gap by focusing on Iran, a developing economy with distinct corporate governance challenges and gender dynamics.

Iran presents a unique setting for examining the relationship between audit committee gender diversity and firm financial performance due to its distinct regulatory, cultural, and economic landscape. Governed by Islamic principles and constrained by economic sanctions, Iran’s corporate governance framework differs significantly from other developing economies yet remains underexplored in the context of gender diversity [25,26]. Deep-rooted gender disparities, patriarchal tendencies, and collective cultural norms influence women’s presence in corporate leadership, Traditional and patriarchal norms impose rigid gender roles that often limit women’s access to professional opportunities and decision-making processes [27]. Family pressures further constrain women by reinforcing traditional roles such as motherhood and household responsibilities, which hinder the pursuit of their professional aspirations [28]. Moreover, social expectations regarding modesty and obedience further restrict women’s individual and professional freedoms [29]. In addition to these cultural and social factors, Iran’s legal and institutional framework plays a critical role. Islam, as the religion of the majority, acknowledges women’s economic independence and legitimizes their employment, if family roles and principles such as modesty and chastity are observed [30]. However, Article 1117 of the Iranian Civil Code grants husbands the authority to prevent their wives from engaging in occupations deemed incompatible with family interests or dignity [31,32]. Although this law does not absolutely prohibit women from working, it is considered a structural constraint that limits their opportunities to participate fully in economic and managerial activities. The country consistently ranks among the lowest in the Global Gender Gap Index, with the World Economic Forum (2024) reporting the lowest parity in labor force participation worldwide [33]. According to the World Bank (2022), women account for only 19.2% of senior and middle management positions in Iran [34]. Moreover, female labor force participation remains extremely low worldwide −15%—compared to both global and regional averages [35]. Unlike many developed economies with legal quotas for female representation, Iran has no statutory requirement for women’s inclusion on boards or committees. This institutional environment makes women’s presence in audit committees largely dependent on voluntary or informal corporate practices [36]. Given these structural and cultural barriers, this study investigates how gender diversity in audit committees influences firm performance, contributing to the broader discourse on corporate governance in emerging markets.

These cultural, social, and legal barriers have resulted in minimal female representation in Iranian corporate governance, with women occupying less than 5% of board seats and appearing only sporadically in audit committees [37]. This situation raises a critical research question: can even minimal female participation in audit committees influence corporate financial and market performance in such a restrictive environment? By focusing on Iranian listed companies, this study addresses a major gap in the literature by exploring gender diversity in audit committees within an emerging economy lacking gender quotas. The limited presence of women in these key committees suggests that their inclusion may be largely symbolic, providing a natural context to examine the implications of tokenism theory in shaping board dynamics.

We develop our hypothesis based on Kanter’s [38] theory of tokenism, which suggests that in environments where cultural, social, and institutional barriers restrict women’s participation in corporate management, their presence on boards and committees is often symbolic rather than influential. In Iran, most firms with female audit committee members typically have only one woman on the committee [39,40], reflecting structural constraints rather than a genuine commitment to diversity. This aligns with tokenism theory, indicating that women's inclusion is more of a compliance gesture than a driver of meaningful change. Consequently, we expect that the presence of women on audit committees in Iranian firms will be largely symbolic and unlikely to have a significant impact on financial performance.

Using a panel dataset of 1058 firm-year observations from the TSE (2013–2019), our findings indicate that the presence of at least one female manager on the audit committee has a positive and significant impact on firm financial performance. These results highlight the importance of gender diversity in audit committees, especially in environments characterized by gender disparities, collectivism, patriarchal structures, and weak corporate governance mechanisms in developing economies. Contrary to [15], our findings support those of [6,24], demonstrating the positive impact of board committee gender diversity on firm performance. Our results remain robust after controlling endogeneity and employing alternative gender diversity measures.

This study presents important implications for policy, practice, and research. First, it contributes to the corporate governance literature in developing economies by addressing the largely overlooked topic of gender diversity in board committees, particularly in Iran. While extensive research exists on board gender diversity, little attention has been given to its impact within key subcommittees. Our findings enhance the understanding of how women’s presence in audit committees influences firm performance. Second, despite the relatively low representation of women in Iranian audit committees compared to both developed and developing nations [37,39,40], our results indicate that even minimal female participation can positively impact financial performance, aligning with prior studies [5,18,41]. Third, our findings highlight that gender diversity can yield financial benefits even in the absence of mandatory quotas, offering valuable insights for policymakers in Iran and other developing economies seeking to reduce barriers to women’s participation in corporate governance. Finally, this study underscores the broader significance of gender diversity, signaling to regulators and policymakers the potential advantages of promoting female representation in boardrooms through legislative measures or voluntary initiatives.

The remainder of this paper is structured as follows: Section 2 presents the theoretical foundation, literature review, and research hypothesis. Section 3 details the data and methodology. Section 4 discusses empirical findings, results analysis, and robustness checks. Finally, Section 5 provides a summary and conclusions.

One of the prominent theories in this field is Dawson’s gender theory [42], which posits that men and women possess distinct values, leading to differing attitudes and behaviors. For instance, men tend to exhibit a greater inclination toward competitive situations [43]. In contrast, women are generally more conservative and demonstrate lower self-confidence [44,45], which may reflect their higher moral reasoning and ethical sensitivity [46]. While men are often perceived as more adept at problem-solving, women frequently provide superior solutions [47]. Furthermore, women are more likely to make ethical decisions and engage in fewer unethical behaviors compared to men [48]. A thorough understanding of this theory is crucial, as it not only contributes to a deeper comprehension of the psychological differences between men and women but also highlights how these behavioral differences significantly influence the decision-making processes of corporate boards [49]. Dawson’s gender theory emphasizes inherent differences between men and women in shaping attitudes and behaviors, yet its applicability in Iran is limited. Despite women’s increasing educational attainment, their representation on boards and audit committees remains low, and patriarchal norms, collectivist culture, and the absence of quota policies or institutional support constrain their ability to influence managerial decisions [37,39,50–52]. These limitations indicate that the essentialist assumptions of Dawson’s theory overlook the critical role of institutional and cultural barriers in shaping gendered outcomes.

The resource dependence theory also offers valuable insights into the impact of gender diversity on board effectiveness. Women bring diverse resources to the board, including expertise, competencies, and leadership experiences [53]. Firms often seek board members who can complement their existing resources and contribute new forms of human and social capital [54]. According to this theory, boards with diverse characteristics, including gender diversity, serve as critical resources. They establish valuable connections with the external environment, which is often uncertain, and facilitate the acquisition of essential resources by maintaining strong relationships with external stakeholders [55,56]. In essence, this theory underscores the importance of gender diversity on boards, as it views women managers as providers of unique resources. Ignoring their talents may lead firms to lose their competitive advantages [10]. Resource dependence theory emphasizes the strategic value of female directors as providers of unique human and social capital. However, in Iran, institutional and cultural barriers limit the extent to which these resources can be mobilized. Although women who reach audit committees often possess exceptional qualifications, structural disadvantages—such as restricted professional networks and weak institutional support—constrain their influence [57]. Moreover, Iran’s collectivist culture fosters conformity and majority–minority dynamics, reducing the effectiveness of gender-diverse groups [39,58]. Thus, despite the theoretical promise of resource dependence theory, contextual realities in Iran suggest that women’s presence in audit committees may not necessarily translate into meaningful performance improvements.

Social and ethical theories further support the inclusion of women on corporate boards. These theories emphasize the moral imperative of ensuring women’s participation in boardrooms and challenge the exclusion of women based on gender [10,59]. Advocates of these perspectives argue that increasing women’s presence on boards contributes to a more just and equitable society [24] and contend that promoting women’s representation on boards is essential for reducing discrimination and fostering fairness among top-level executives [59]. Beyond ethical considerations, gender diversity enhances decision-making, creativity, and innovation, as individuals with diverse backgrounds bring varied perspectives to the table [60]. However, prior research [10] caution that if women’s inclusion on boards is driven solely by social or moral pressures rather than competence, it may undermine board effectiveness, diminish firm value, and even lead to negative valuations in financial markets [61]. Social and ethical theories emphasize the normative imperative of women’s inclusion in decision-making bodies, highlighting justice, fairness, and equality. However, in practice, institutional and cultural barriers in Iran, as well as in countries such as Turkey and Sub-Saharan Africa, often render women’s participation largely symbolic [24,62,63]. The absence of gender quotas, patriarchal norms, and limited legal protections hinder the practical realization of these normative principles, demonstrating that moral imperatives alone are insufficient; without institutional and cultural support, women’s presence in audit committees and boards frequently fails to exert meaningful influence on corporate decisions and performance.

Kanter’s critical mass [38] theory provides another lens through which to examine gender diversity on boards. This theory suggests that the presence of two or more women on a board can mitigate the effects of tokenism. Supporting this view, research by [41,64] demonstrates that increasing the number of women in boardrooms enhances board dynamics, leading to more effective decision-making and improved firm performance [23]. Studies by [18] reveal that while gender diversity may initially have a negative impact on firm performance, achieving a threshold of 30% or more women on the board results in positive outcomes. Similarly, [4,65,66] find that having three or more women on the board significantly and positively influences firm performance. These discussions gain particular significance in the Iranian context, where many firms have at most one woman on the audit committee [39], making the situation more consistent with the logic of tokenism rather than that of critical mass. Moreover, weak institutional protection of investors [67] and underdeveloped corporate governance mechanisms [68] further constrain the full realization of women’s human and social capital. Therefore, a critical assessment of these theories in this setting suggests that while critical mass theory emphasizes a minimum threshold for women’s influence, its applicability in Iran is limited. Instead, tokenism provides a more suitable framework for explaining the prevailing dynamics.

In summary, the theoretical perspectives reviewed above present mixed evidence regarding the impact of women’s presence on corporate boards. While some theories highlight the potential benefits of gender diversity, others caution against its unintended consequences. This ambiguity underscores the need for empirical evidence which this study aims to provide.

Prior ResearchIn a meta-analysis of 120 studies between 1997 and 2014, [69] show that the presence of women on the board of directors positively affects the firm’s performance. In line with these results, many empirical studies show a positive relationship between gender diversity on the board of directors and the firm’s financial performance [6,9–12,65]. However, other studies find the existence of a significant relationship between the gender diversity of the board of directors and the performance of the firm has not been reported [14,66,70–72]. Several studies found a negative relationship between the gender diversity of the board of directions and the performance of the firm [19,73–76] was observed. Based on these contradictory and mixed results, there seems to be no consensus on the effects of gender diversity on firm performance. At the same time, it can question theoretical approaches to the advantages of women on the board of directors and its sub-committees. Brammer S, et al. [59] argue that female representatives on the directors’ board must be viewed as a procedure to degrade the existing discrimination and detect injustice from the firm’s top managers as a perfect target. Women provide a wide range of resources, including expertise, competence, and various managerial experiences, and when such human capital is ignored, it will adversely affect the efficiency of the firm and likely lose its competitive advantage [6,77]. There are also legal requirements for gender equality (e.g., Norway, Spain, Finland) or strong recommendations for the presence of women on the directors’ board of firms (e.g., Australia, Denmark, Germany) in their agenda [7,8]. Many prior studies are conducted in developed countries in Europe and North America, and only a small number of studies have been carried out in developing countries [24,57,78] with the focus on the effects of female representatives on the audit committee and the performance of the firm [6,15,79]. This paper contributes to the extant literature by investigating the association between female directors and firm performance in a developing country such as Iran.

Hypothesis DevelopmentThis study explores the impact of gender diversity in audit committees on the financial performance of firms in Iran, a country facing distinct cultural, social, economic, and institutional challenges that shape this relationship. These challenges not only limit women’s presence in managerial roles but also contribute to tokenism as the symbolic inclusion of women in audit committees without real influence. Several key factors reinforce this phenomenon. First, gender, religious, legal, and institutional barriers significantly restrict women’s advancement. World Economic Forum 2022 [80] highlights Iran’s gender gap in managerial positions, while traditional religious interpretations, societal norms, and legal constraints, such as Article 1117 of the Iranian Civil Code, further limit women’s leadership roles. Weak institutional structures and the absence of legal mandates for female representation in audit committees allow companies to take a passive approach toward gender diversity, making appointments largely symbolic. Second, cultural and social norms, rooted in Iran’s patriarchal and collectivist society [81], hinder women’s influence in strategic decision-making. Prior research suggests that collectivist cultures prioritize group conformity over diversity, weakening the impact of minority representation [82], while patriarchal norms further diminish the benefits of gender diversity on firm performance [19]. Third, Iran’s weak capital market and lack of corporate transparency [68,83] reduce the external pressure on firms to genuinely embrace gender diversity, as investor protections remain weak [21]. Finally, managerial and organizational structures contribute to women’s underrepresentation, with women holding only 4.5% of board seats in Iranian firms [37] and being largely absent from audit committees—appearing as the sole female member in many cases or entirely excluded in 41.87% of surveyed firms [39,40]. These structural and cultural barriers reinforce tokenism, ultimately shaping the role of gender diversity in Iranian corporate governance.

This trend indicates that women’s appointments to audit committees in Iranian firms are largely symbolic rather than a genuine effort to enhance their decision-making influence. According to Critical Mass Theory, firms with fewer than three women on their boards often fail to realize the benefits of gender diversity due to the absence of a critical mass [18]. Minimal female representation in corporate governance, without reaching this threshold, has limited impact on improving organizational performance. Similarly, Tokenism Theory [38] suggests that when women are significantly underrepresented in decision-making bodies, their roles tend to be symbolic, restricting their ability to influence managerial decisions. This is evident in Iranian firms, where women’s presence on audit committees is often limited to the bare minimum, preventing them from exerting meaningful oversight on financial and governance matters. Furthermore, prior research indicates that tokenism can undermine board effectiveness by fostering isolation and discouraging challenges to dominant perspectives [23,66,84]. It may also lead to the perception that female audit committee members are included merely to satisfy diversity expectations rather than to contribute substantively, further limiting their influence on firm strategies [6]. As a result, token representation fails to drive meaningful improvements in corporate performance and instead reinforce existing power dynamics. Based on these considerations, this study proposes the following hypothesis:

Hypothesis (H1). The presence of women on the audit committee does not have a significant impact on the financial performance of Iranian firms.

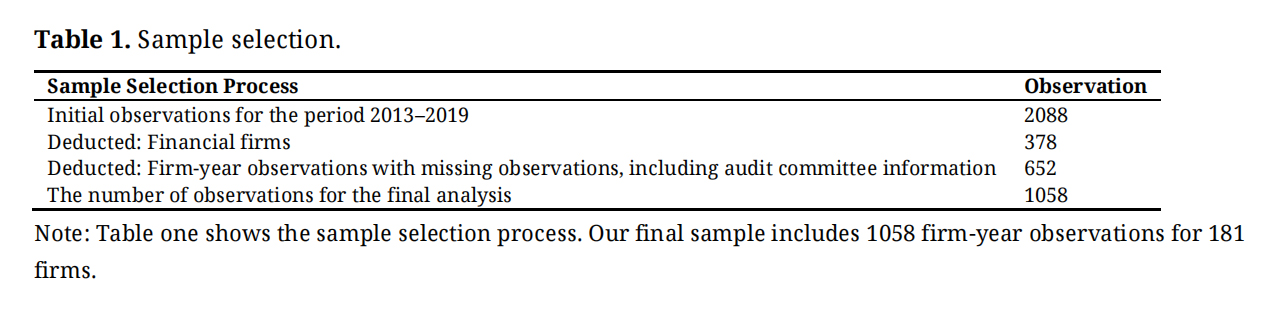

The sample includes all firms listed on the TSE from 2013 to 2019. The study period was set from 2013 to 2019. The year 2013 was selected as the starting point because the TSE issued internal control guidelines that mandated the establishment of audit committees in all listed firms, thereby creating a unified regulatory framework for corporate governance practices in Iran. The year 2019 was chosen as the endpoint, since from 2020 onwards, the outbreak of the COVID-19 pandemic generated extraordinary economic and operational disruptions that could confound the findings. Previous studies have confirmed that the pandemic substantially influenced firm performance and governance both globally [85,86] and in the Iranian capital market [87]. Therefore, focusing on the period 2013–2019 ensures the reliability and comparability of the data within a stable institutional and economic context. All the necessary information for this research was manually extracted from the comprehensive database of the Iran Securities Exchange Organization (CODAL) (CODAL is the official platform for the disclosure of information by companies listed on the TSE. All data on this platform are freely accessible to the public, including academic researchers, and are not subject to copyright restrictions.). Specifically, data related to the audit committee was collected from the comprehensive audit committee reports available in CODAL. Information regarding the board of directors, ownership structure, firm age, and other research variables was obtained from the board of directors’ reports and financial statements in the database. Firm-year observations related to financial firms were excluded due to their distinct internal control procedures [40,88] and differences in corporate governance regulations [24]. Additionally, firms and firm-years with missing data required for model estimation were removed. As a result, the final sample consisted of 1058 firm-year observations for 181 firms. The sampling method is described in Table 1.

Table 1. Sample selection.

Table 1. Sample selection.

To investigate the research hypothesis based on the effect of women’s participation in audit committees on the firm’s performance, we estimate the research model as follows:

Research model

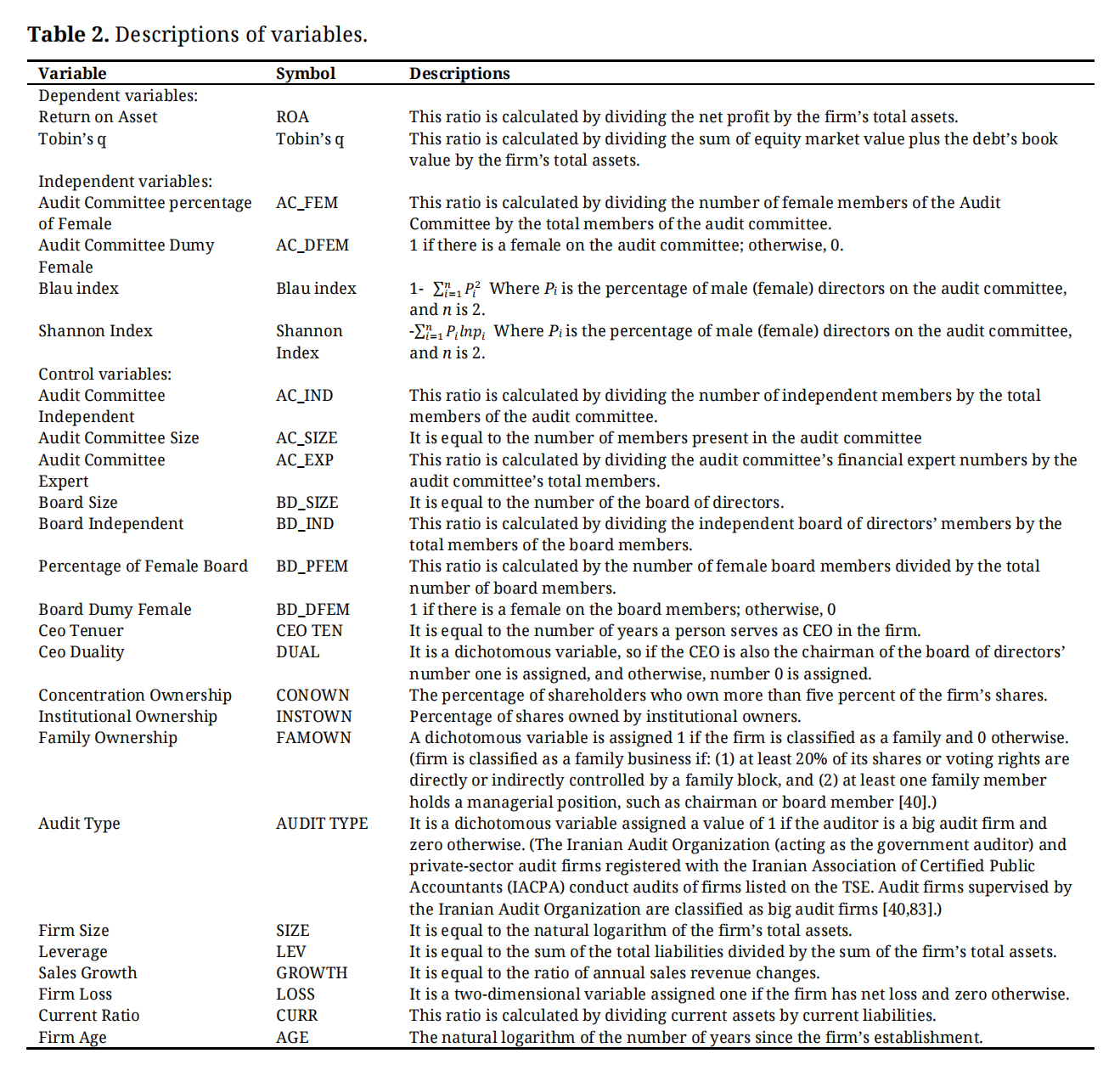

Dependent VariableThis research employs return on assets (ROA) and market-based performance criteria to assess a firm’s financial performance. The ROA measure may be influenced by accounting contracts and subject to management manipulation. To further reinforce the results, we incorporate the Tobin-Q index, which reflects market expectations of the firm’s future profitability. This index aligns with prior research [6,12,24] examining the relationship between corporate governance—specifically, the board of directors and the audit committee—and a firm’s financial performance.

Independent VariablesFollowing prior studies [6,24], we define gender diversity (AC-FEM) as the proportion of women on the audit committee relative to its total members. Additionally, we introduce a dummy variable, AC-DUMFEM, which equals 1 if at least one woman is present on the committee and 0 otherwise [40].

Control VariablesTo isolate the net effect of gender diversity in audit committees on firm performance, this study incorporates a comprehensive set of control variables related to corporate governance, ownership structure, audit committee characteristics, auditor type, and firm-specific attributes. Prior research has consistently confirmed the strong link between governance mechanisms and financial outcomes [89]. Board size is considered one of the most important control variables, as the number of directors can directly influence decision-making efficiency and effectiveness. Larger boards may provide greater diversity of resources, enhanced external links, and stronger monitoring capacity; however, excessively large boards can create coordination problems and increase agency costs, ultimately undermining effectiveness [57]. Board independence is also a key governance factor. A higher proportion of independent directors typically enhances monitoring, reduces managerial dominance, and safeguards shareholder interests, whereas limited independence may weaken oversight [90–92]. In this study, board independence is measured as the percentage of independent directors.

Audit committee characteristics are also included among the control variables. Financial expertise of audit committee members plays a critical role in improving the quality of financial reporting and oversight functions [93,94]. Here, financial expertise is measured as the percentage of members with financial expertise. Audit committee independence is likewise essential, as independent members are more inclined to challenge management and ensure effective monitoring [95,96]; this is defined as the percentage of independent audit committee members. Drawing on resource dependence theory, audit committee size can enhance supervision and firm performance by providing diverse expertise, although excessively large committees may weaken oversight and reduce effectiveness [58,93,95]. Accordingly, audit committee size is measured as the total number of committee members.

Ownership structure is another crucial determinant of firm outcomes. Institutional ownership generally exerts a positive influence, as institutional investors often have the ability and incentives to monitor management effectively [97,98]. In contrast, family ownership and ownership concentration may yield mixed effects: while they can align managerial and majority shareholder interests, they may also heighten the risk of expropriating minority shareholders [99–102]. CEO duality (when the CEO simultaneously serves as board chair) is also controlled for, since it may concentrate power and reduce board independence, thereby weakening firm performance [21]. This variable is coded as a dummy (1 if CEO duality exists, 0 otherwise). CEO tenure is also included, as longer-serving CEOs may benefit from firm-specific knowledge but may also become entrenched and resistant to change [21]. From a financial perspective, leverage (total debt to total assets) is included as a key indicator. While leverage can discipline managers by imposing repayment obligations, excessive leverage raises bankruptcy risk [24].

Firm size is measured as the natural logarithm of total assets, capturing potential benefits of economies of scale and access to financial resources, while also acknowledging possible bureaucratic inefficiencies [10,103]. Firm age, measured as the number of years since listing on the TSE, is controlled for, as older firms may benefit from accumulated experience and reputation but may also suffer from organizational inertia [4]. Additionally, sales growth is included to capture growth opportunities [75]; auditor type is incorporated as a proxy for audit quality; loss indicator is added to account for financial distress; and the current ratio is included to measure short-term liquidity. Finally, industry and year fixed effects are employed to control sectoral heterogeneity and time-specific influences. Despite the comprehensive set of controls employed in this study, several potentially important variables could not be incorporated due to data limitations. For instance, organizational culture [104,105], managerial ability [106], and firms’ innovation intensity [107] have been shown to significantly influence financial outcomes. Moreover, institutional and macro-level factors, such as regulatory restrictions and economic sanctions, may also affect firm performance. While the omission of these factors could bias estimates if correlated with both gender diversity and firm performance, the extensive set of governance and firm-level controls included in the model mitigates this concern. Future research using richer datasets could explicitly account for these omitted variables. Table 2 provides the full classification and measurement of all research variables.

Table 2. Descriptions of variables.

Table 2. Descriptions of variables.

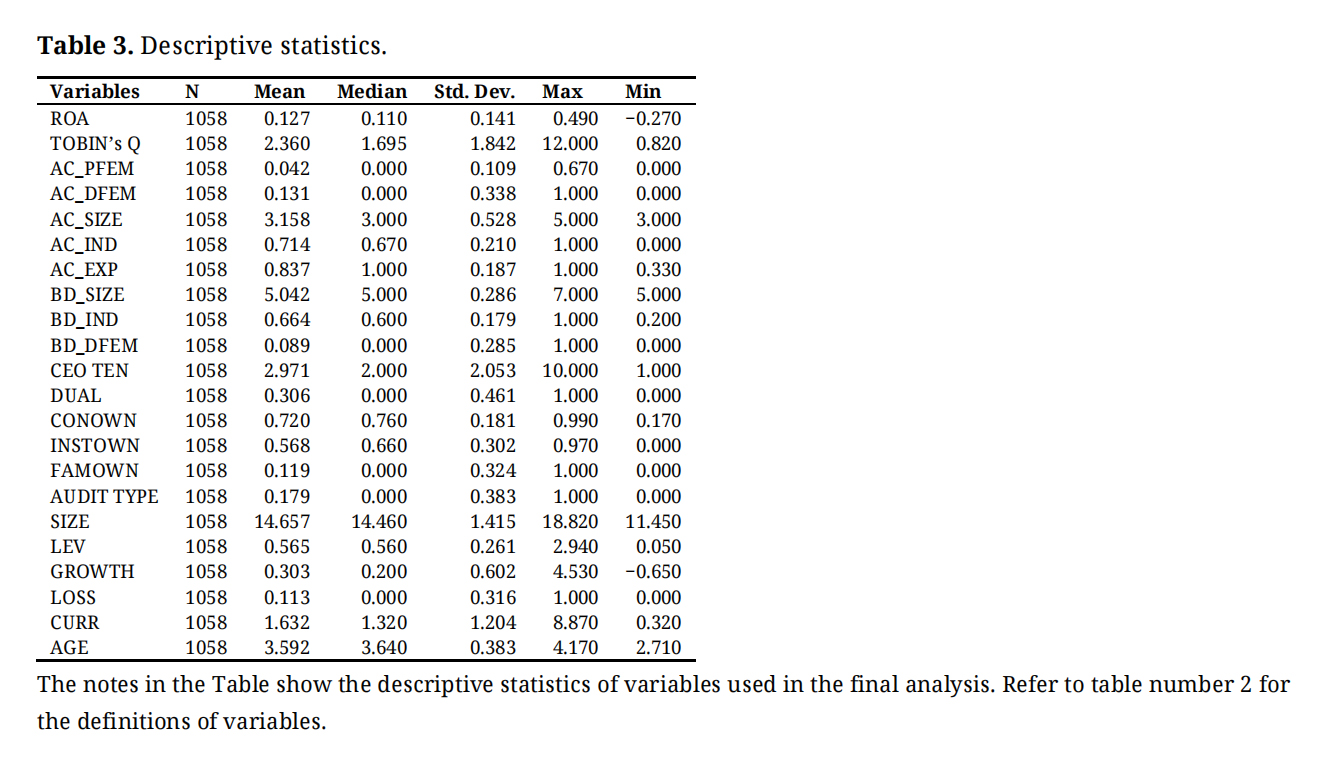

Table 3 presents the descriptive statistics of the research variables. The ROA index has an average of 0.127 and a median of 0.110. Additionally, the average Tobin’s Q index is 2.360. The average percentage of female members on the audit committee is 0.042, while 0.131 of the audit committees in firms listed on the TSE have at least one female member. The average size of the audit committee is 3.158 members, with a minimum of 3 and a maximum of 5. The results indicate that 0.714 of the audit committee members are independent. Furthermore, an average of 0.837 committee members have financial expertise. The average number of board members is 5.042, of whom 0.664 are independent, and only 0.089 are women. The results also show that the average CEO tenure in Iranian firms is 2.971 years, while 0.306 of CEOs also serve as the chairman of the board of directors. Regarding ownership structure, the average ownership concentration, institutional ownership, and family ownership are 0.720, 0.568, and 0.119, respectively. Approximately 0.179 of the sample firms are audited by large audit firms. Additionally, the average firm size is 14.457, the average debt ratio is 0.565, and the average growth rate is 0.303. Lastly, 0.113 of the firms have reported financial losses.

Table 3. Descriptive statistics.

Table 3. Descriptive statistics.

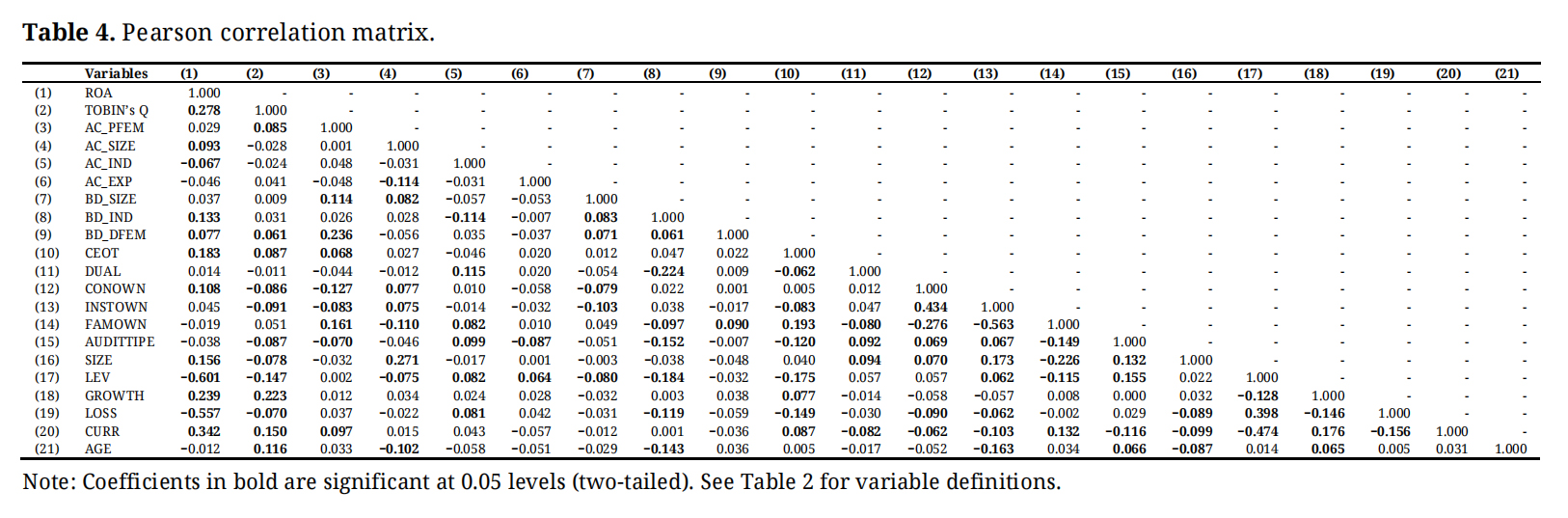

Table 4 reports the Pearson correlation coefficients among the variables. We observe a positive and significant correlation between Tobin’s Q index and the percentage of female audit committee members. The independent variables show low correlation coefficients, the highest being 0.434 and −0.563, indicating that a high linear correlation is not a concern. This is further confirmed by the variance inflation factors (VIF), with all values below 5 and an average of approximately 1.7, suggesting that multicollinearity is not a serious problem in our models.

Table 4. Pearson correlation matrix.

Table 4. Pearson correlation matrix.

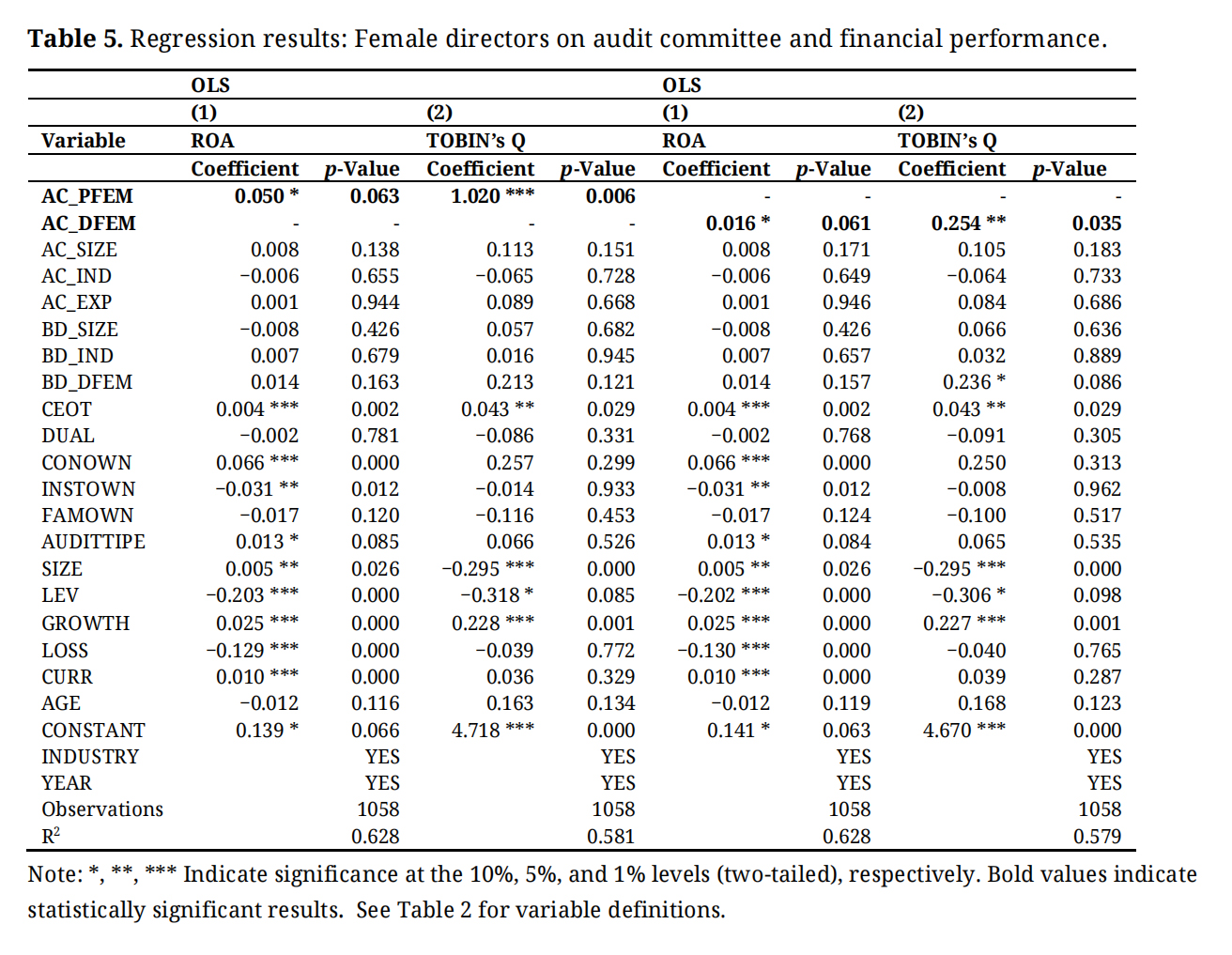

Table 5 presents the Ordinary Least Squares (OLS) regression results on the impact of women’s participation in the audit committee on the firm’s financial performance, using ROA and Tobin’s Q indices. The results indicate a positive and significant correlation between the proportion of women in the audit committee and the firm’s financial performance in columns one and two (ROA: β = 0.05, p < 0.10; Tobin’s Q: β = 1.02, p < 0.01). Similarly, the results show a positive and significant relationship between the dummy variable for female presence in the audit committee and the firm’s financial performance (ROA: β = 0.01, p < 0.10; Tobin’s Q: β = 0.25, p < 0.05). In other words, the findings suggest that a 1% increase in the presence of women on the audit committee leads to a 5% increase in ROA and a 1.02% increase in Tobin’s Q. These results reject the research hypothesis and instead confirm that the presence of women on the audit committee of Iranian firms has a positive and significant effect on financial performance. To examine the presence of heteroscedasticity in the regression model, the Modified Wald Test was conducted, and the results indicated the existence of heteroscedasticity. Furthermore, to detect potential autocorrelation among the model errors, the Wooldridge test was applied, which confirmed the presence of autocorrelation. To ensure the robustness of the findings and to address these issues, the regression was re-estimated using the Generalized Least Squares (GLS) method. The comparison of the GLS and OLS coefficients revealed no significant differences, indicating that the OLS-based results are both stable and reliable.

These results are not only statistically significant but also economically meaningful. The positive and significant coefficient of AC_PFEM indicates that even relatively small changes in the proportion of women on audit committees can lead to tangible improvements in firm performance. For example, a one- percentage-point increase in female presence is associated with approximately a 5% increase in ROA, a figure that is highly relevant for managers and shareholders in terms of profitability and financial efficiency. Similarly, an increase of more than one unit in Tobin’s Q suggests that the market also reacts positively to women’s participation in audit committees, interpreting it as a signal of improved corporate governance quality. In addition, the coefficient of AC_DFEM confirms that the presence of even a single woman on the audit committee is sufficient to generate a significant economic effect on firm performance. These findings demonstrate that the outcomes obtained are not limited to statistical implications but underscore that gender diversity in audit committees can serve as a practical and applicable mechanism for improving financial performance and enhancing firm value. Such evidence is consistent with resource dependence theory as well as prior studies highlighting the role of gender diversity in strengthening corporate governance quality.

The positive and significant coefficients are both statistically and economically meaningful. Even a one-percentage-point increase in female audit committee representation corresponds to roughly a 0.05-point rise in ROA—about a 5% improvement relative to the sample mean—and more than a one-unit increase in Tobin’s Q, signaling stronger governance to the market. These magnitudes align with findings for European firms [5] and Nigerian companies [24], while differing from U.S. and Scandinavian evidence reporting neutral or negative effects [15,17–19]. This contrast suggests that in emerging markets like Iran—where governance mechanisms are weaker and gender disparities are pronounced—even limited female participation can substitute for deficient oversight and yield tangible gains for managers, shareholders, and policymakers. From a theoretical perspective, the results support resource dependence theory but contradict Kanter’s critical mass theory [38]. According to this theory, having a small percentage of women in the audit committee may merely serve as tokenism rather than contributing to substantial changes. Surveys conducted by [39,40] reveal that some Iranian firms with gender-diverse boards and audit committees often have only one female member, reinforcing this concern. The findings can be explained by the fact that in Iran’s underdeveloped corporate governance environment, female audit committee members may positively influence financial performance by leveraging their expertise, competence, and management experience as an alternative to weak governance structures. However, these results should be further validated through robustness tests. As expected, the study also confirms that control variables, including CEO tenure (CEO TEN), ownership concentration (CONOWN), institutional ownership (INSOWN), firm size (SIZE), financial leverage (LEV), growth rate (GROWTH), and current ratio (CURR), are significantly related to the firm’s financial performance.

Table 5. Regression results: Female directors on audit committee and financial performance.

Table 5. Regression results: Female directors on audit committee and financial performance.

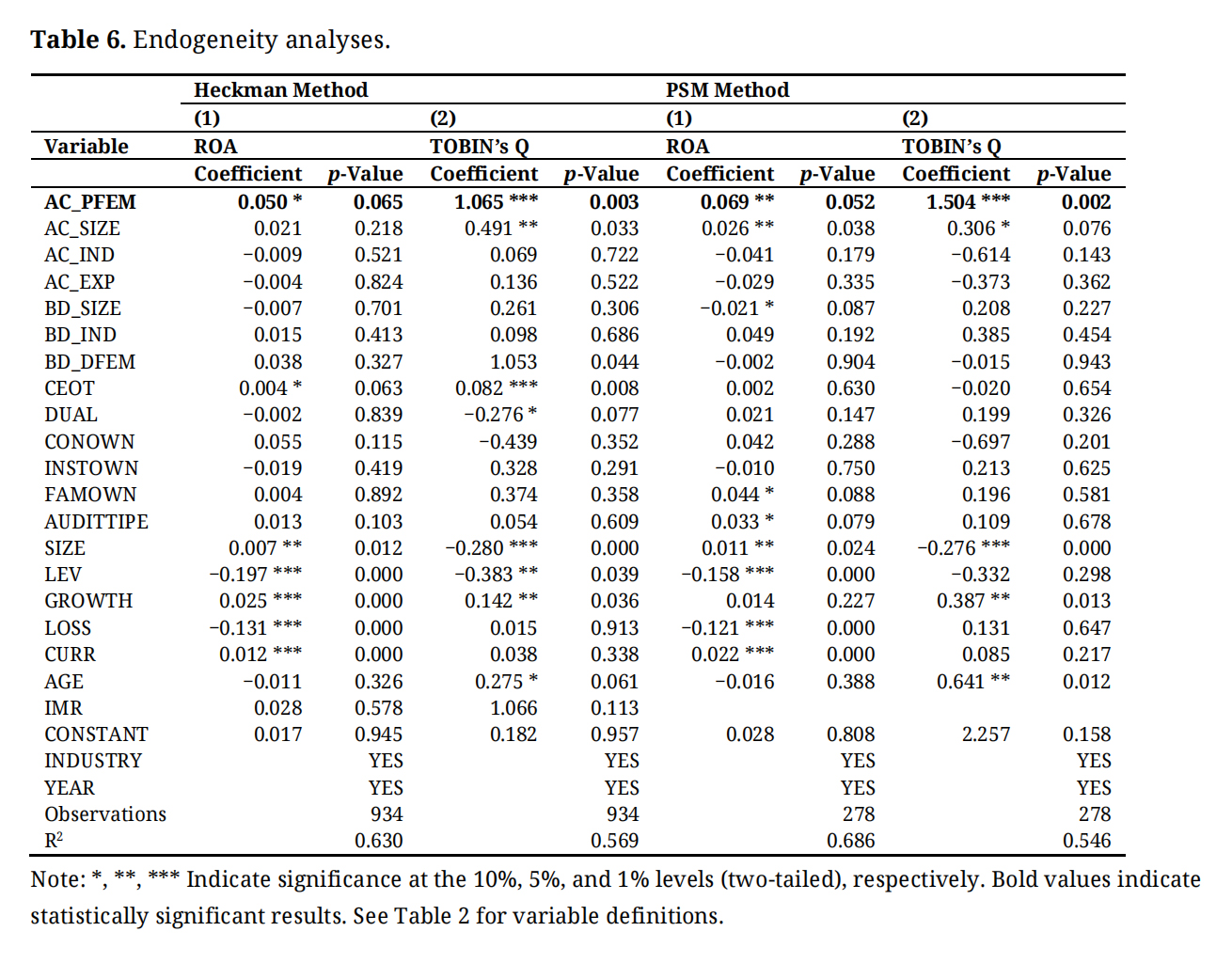

Considering the significant concerns about endogeneity in corporate governance research—particularly in studies involving boards of directors and their committees, the regression model results may be misleading [6,24]. Specifically, firms with gender-diverse audit committees (i.e., those with at least one female member) may have inherently different characteristics compared to firms without gender diversity in their audit committees. Consequently, the financial performance of these firms may be influenced by these characteristics rather than by gender diversity itself. To mitigate potential endogeneity concerns, we follow prior research and employ two methods: Propensity Score Matching (PSM) [40,104,105] and Heckman’s (1979) two-step procedure [106,107] to control for selection bias.

PSM ensures that firms with at least one female member in the audit committee (the treatment group) are matched with firms without female representation in the audit committee (the control group) based on similar characteristics. The PSM process consists of two stages:

1.

2.

Our sample consists of 278 firm-year observations, derived from an initial sample of 139 firm-year observations of firms with at least one female member on the audit committee. The unreported findings indicate no significant difference in the average values of variables affecting the selection of a woman in the audit committee between the treatment and control groups, confirming successful matching in the first stage. The second-stage outcome model results are presented in Table 6, showing that our main findings remain robust to endogeneity concerns (ROA: β = 0.069, p < 0.10; Tobin’s Q: β = 1.504, p < 0.01). These results confirm that gender diversity in the audit committee is not significantly influenced by endogeneity.

The second method to address potential endogeneity concerns is Heckman’s (1979) two-step process. This approach corrects for potential self-selection bias by incorporating the inverse Mills ratio into the regression model.

3.

4.

Based on these findings, we conclude that self-selection bias does not affect our main analysis, and our results are not driven by endogeneity.

Table 6. Endogeneity analyses.

Table 6. Endogeneity analyses.

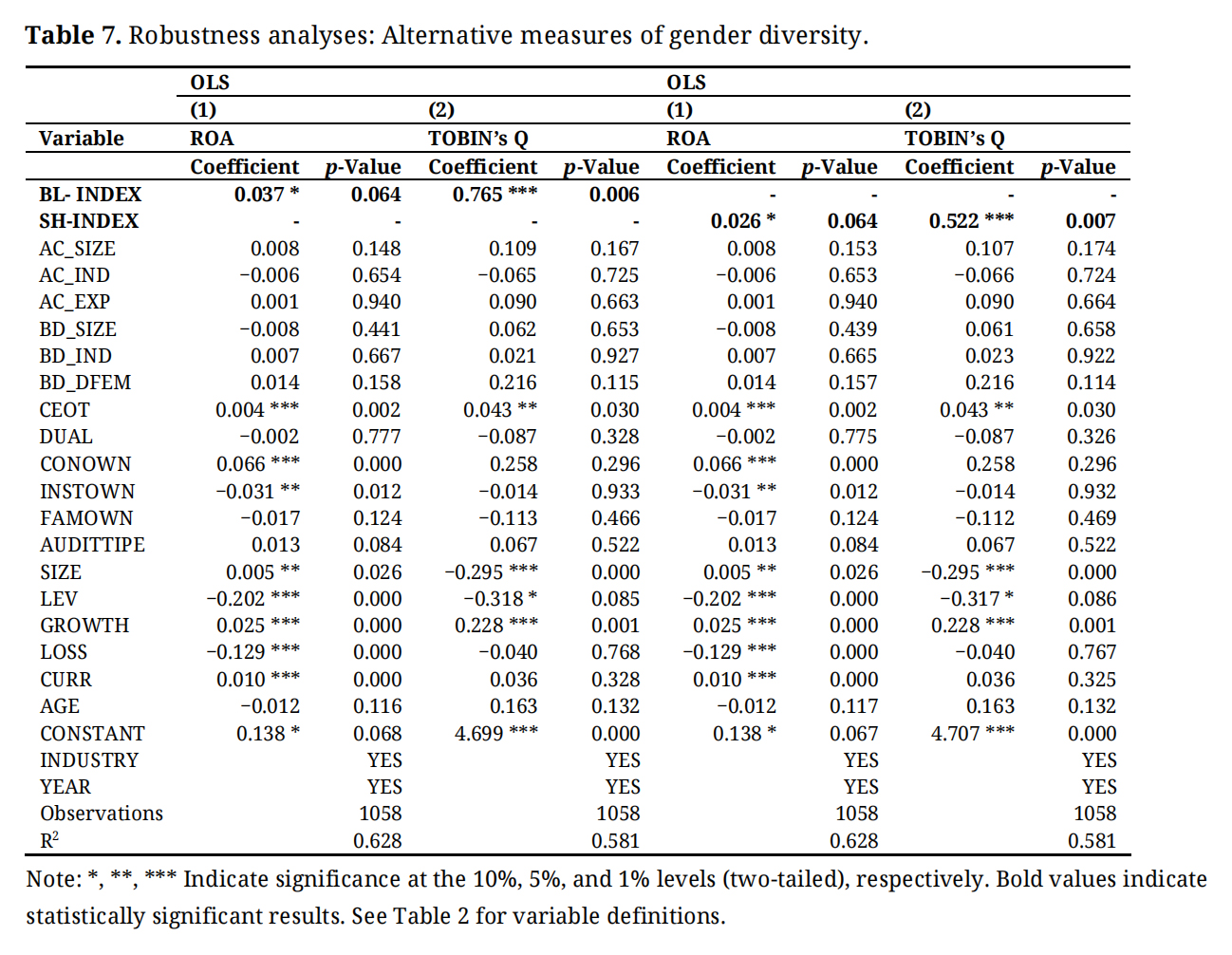

To ensure the robustness of our research findings and in line with previous research on gender diversity [11,108,109], we adopt a two-step approach using alternative criteria for gender diversity, including the Shannon index and the blue index. The definitions of these indicators, as presented in Table 2, align with the research framework. As shown in Table 7, the coefficients for both the blue index (ROA: β = 0.037, p < 0.10; Tobin’s Q: β = 0.756, p < 0.01) and the Shannon index (ROA: β = 0.026, p < 0.10; Tobin’s Q: β = 0.522, p < 0.01) are positive and significant. These findings align with our main results and confirm the robustness of our conclusions. To ensure the accuracy of the results and to address potential econometric issues, heteroscedasticity was examined using the Modified Wald Test, and autocorrelation of the errors was assessed with the Wooldridge test, both of which indicated the presence of these problems. Accordingly, the regressions were re-estimated using the GLS method. The results showed that the GLS coefficients did not differ significantly from the OLS coefficients, indicating the stability and reliability of the main results as well as the robustness test outcomes.

Table 7. Robustness analyses: Alternative measures of gender diversity.

Table 7. Robustness analyses: Alternative measures of gender diversity.

This study investigates the relationship between gender diversity in audit committees and firm financial performance in the context of Iran—a developing economy characterized by patriarchal structures, weak corporate governance, and notable gender disparities. While rooted in the tokenism theory, which predicts limited influence from symbolic female representation, our empirical findings contradict this view and instead offer strong support for the resource dependence theory. The regression results, robust across various model specifications and endogeneity controls (including PSM and Heckman methods), reveal a consistent and significant positive association between female presence in audit committees and both accounting-based (ROA) and market-based (Tobin’s Q) performance measures. These findings challenge Kanter’s critical mass theory, which posits that a threshold of at least three women is necessary to yield meaningful influence. In contrast, our study shows that even minimal female participation—as low as a single member—can enhance audit committee effectiveness in a context of weak governance structures. This supports prior findings by [6,24,64], who argue that gender-diverse boards and subcommittees contribute to improved firm oversight and decision-making, even in collectivist or hierarchical settings.

From a theoretical perspective, these results underline the value of resource dependence theory in explaining the strategic importance of female audit committee members. Despite institutional constraints in Iran—including limited legal mandates for female representation, low investor protection, and male-dominated corporate culture—women’s participation appears to offer complementary expertise and governance capacity that positively affect firm performance. This is aligned with arguments from [10,53,55], who emphasize that diverse boards improve firm access to external resources, legitimacy, and stakeholder trust. Moreover, our results indicate that in weak institutional environments, the symbolic inclusion of women may paradoxically generate real economic benefits. While tokenism theory assumes marginalization, our findings suggest that in settings with underdeveloped governance mechanisms, even symbolic inclusion can serve as a catalyst for improved monitoring, risk mitigation, and strategic balance. Beyond merely confirming resource dependence theory, our findings extend tokenism theory by demonstrating that, in contexts of weak corporate governance, even the symbolic presence of women can generate meaningful governance benefits. We term this phenomenon “contextual tokenism”—a situation in which the limited presence of women provides scarce monitoring capacity, reputational capital, and external linkages, partially substituting for ineffective formal controls. This result challenges the universal applicability of critical mass theory, suggesting that substantial performance improvements can occur without reaching the conventional threshold of three women or 30% female representation.

This insight expands the scope of existing research by demonstrating that token representation may still create tangible firm-level outcomes, especially when traditional oversight mechanisms are absent or ineffective This paper thus makes a distinct contribution to the existing literature by refining tokenism theory for emerging-market contexts and demonstrating that minimal representation can still enhance governance effectiveness. Consistent with prior studies [5,12,24], our findings should therefore be interpreted as statistical associations rather than direct evidence of committee processes. Nevertheless, female audit committee members may plausibly enhance governance effectiveness by strengthening oversight, enriching board deliberations through diverse perspectives, and promoting greater transparency in financial reporting. Although our dataset does not capture such internal mechanisms directly, these theoretical pathways provide a reasonable explanation for the observed positive association between women’s participation and firm performance, and future qualitative or mixed-method studies could explore them more explicitly. Ultimately, our results suggest that gender diversity in audit committees plays a critical role in enhancing corporate sustainability by strengthening governance quality and financial performance, improving oversight, and fostering a broader perspective in decision-making. Female directors bring unique insights, ethical sensitivity, and a stronger inclination toward transparency and accountability, which can translate into more rigorous monitoring of financial reporting, risk management, and sustainability practices. Diverse audit committees are more likely to challenge management effectively, encourage long-term strategic thinking, and ensure that environmental, social, and governance (ESG) sustainability issues are integrated into corporate policies. This inclusive governance structure enhances stakeholder trust and promotes responsible business practices that support sustainable growth and resilience in the face of economic, social, and environmental challenges.

The practical implications of these findings are particularly relevant in Iran’s regulatory and cultural context. Although the audit committee charter was first issued in 2012 following article 10 of the 2012 Internal Control Guidelines, and the establishment of audit committees for all listed firms became mandatory, neither this charter nor the latest Corporate Governance Code (2023) makes any reference to gender diversity. The results of this study indicate that even minimal female participation in audit committees can enhance financial performance. Therefore, the Securities and Exchange Organization (SEO) could revise the audit committee charter or the 2023 Corporate Governance Code to include gender diversity as a recommended and non-mandatory practice. Complementary measures may include requiring listed firms to disclose the gender composition of their committees in annual governance reports, providing financial incentives and recognition for leading companies, and developing specialized training and certification programs for professional women. These programs can help women overcome limited access to professional networks and managerial experience, build confidence among boards and organizations in their effective participation, and create a more balanced opportunity environment in which structural and cultural barriers have previously constrained women’s involvement. Boards should also recognize gender diversity as a strategic drive for improving oversight, transparency, and investor trust. This gradual and incentive-based approach, aligned with Iran’s cultural values and legal framework, provides a feasible and sustainable pathway to increasing women’s participation in corporate governance.

We acknowledge several limitations in our study. Although endogeneity concerns were addressed and simultaneity was controlled by using propensity score matching (PSM) and the two-stage Heckman approach, unobserved firm-level characteristics such as organizational culture, managerial capabilities, firms’ innovation intensity, or strategic orientation—may still influence the results. In addition, our data did not include direct information on audit committee processes (e.g., number of meetings and agendas) or mediating variables such as audit quality and earnings management. Therefore, the findings should be interpreted with caution and within the specific institutional and governance context of Iran. To enhance the robustness and generalizability of these findings, future research could examine similar dynamics in other emerging Middle Eastern and North African economies or in countries with mandatory gender quotas. Moreover, leveraging richer committee-level data and employing mixed methods (e.g., interviews and case studies), alongside expanding the analysis to ESG sustainability indicators, could provide a more comprehensive and in-depth understanding of the causal mechanisms and the impact of gender diversity on board committees.

The dataset of the study is available from the authors upon reasonable request.

GH designed the study, collected the data, performed the analysis, and drafted the manuscript. ZR critically reviewed the manuscript and contributed to its scientific revision and final approval. All authors read and approved the final version of the manuscript.

The authors declare that there is no conflicts of interest.

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

The authors would like to thank Mr. Javad Oradi, Fakhreddin Mohammadrezaei and Mohammad Alipour for their valuable scientific advice during the preparation of this study.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

64.

65.

66.

67.

68.

69.

70.

71.

72.

73.

74.

75.

76.

77.

78.

79.

80.

81.

82.

83.

84.

85.

86.

87.

88.

89.

90.

91.

92.

93.

94.

95.

96.

97.

98.

99.

100.

101.

102.

103.

104.

105.

106.

107.

108.

109.

Rezaee Z, Haidarinezhad G. Gender diversity in audit committees and firm performance: Insights from a developing economy. J Sustain Res. 2025;7(4):e250065. https://doi.org/10.20900/jsr20250065.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions