Location: Home >> Detail

J Sustain Res. 2025;7(4):e250073. https://doi.org/10.20900/jsr20250073

,

Jitka Meluchová *

,

Jitka Meluchová *

Department of Accounting and Auditing, Faculty of Economic Informatics, Bratislava University of Economics and Business, Bratislava 852 35, Slovakia

* Correspondence: Ján Vlčko, Jitka Meluchová

This study aims to determine the impact of an economic crisis on the quality of disclosed financial figures in balance sheet and profit and loss (P&L) statements. Recently, the COVID-19 pandemic caused a global economic crisis, providing a unique opportunity to examine its impact. In the European Union, the requirements for disclosing information in financial statements depend on the enterprise size group. EU directives categorize enterprises into four (or three) size groups. In this study, we demonstrate that the quality of disclosed balance sheets and P&L in financial statements prepared according to the International Financial Reporting Standards and for small enterprises is acyclical, that for micro enterprises it is cyclical, and that for large enterprises it is countercyclical. The results provide significant information not only for financial statement users but also for policymakers and regulatory bodies.

EU, European Union; IFRS, International Financial Reporting Standards; P&L, Profit and Loss statement; ROA, Return on Assets; ROE, Return on Equity; QR, Quick ratio; GR, Revenue growth rate; DER, Debt to equity ratio; CR, Current Ratio.

Financial statements provide complex information to users; however, ref. [1] the main sources for financial analysis are the balance sheet and P&L statements [2]. In recent years, we have faced an increase in the importance of non-financial information being disclosed in financial statements, such as environmental sustainability [3,4]. Yet, financial information remains the main source of information for financial analysis. Therefore, the accounting policies and GAAP shaping a balance sheet and P&L statement should be constantly evaluated, monitored, and discussed on the academic level in order to maintain relevance in providing useful information for various financial statement users. This study contributes to the academic literature by informing financial statement users of an important consideration regarding the effect of the economic cycle on financial statement quality. This research also provides an important methodology for further research, replicable on any market worldwide. Despite the simplicity of the methodology, the results are significant, aiming to further enhance academic discussion regarding accounting trends, or whether principle-based IFRS or scrutinized GAAP are more profound and more useful for the wide spectrum of financial statement users. Financial statements must not only provide a fair presentation for their users; they should also provide comparable information [5]. Financial statement users should be able to obtain comparable information on a microeconomic level [6] comparing at least two reporting periods for a company [7], and they should also, especially capital market investors, be able to compare information among companies [8]. The financial statements of listed companies are subject to audit [9]. The main goal of an audit is to ensure that financial statements provide a fair presentation [10]. According to the IFRS, “an entity achieves a fair presentation by compliance with applicable IFRS” [11]. Local Generally Accepted Accounting Principles (GAAP) require a similar approach [12]; financial statements must comply with all local GAAP for fair presentation [13]. For financial statements that meet all the GAAP requirements, the auditor must notify users that they are providing a fair presentation [14]. Financial statements must provide useful information for users [15]; however, a company can use its professional attitude [16] to determine what information might be useful for financial statement users [17]. Companies use their professional attitudes to recognize, measure, and evaluate the relevant information to disclose in financial statements [18]. IFRS does not require the disclosure of immaterial information [11]. Financial statement users rely on a company’s professional attitude and its auditor for presentation of fair, accurate, and useful information in financial statements [19]. As companies rely heavily on their subjective professional opinions to evaluate and determine the information to disclose in their financial statements [20], it is necessary to examine to what extent an economic crisis affects the quality of financial statements, especially the quality of the financial information disclosed in balance sheets and P&L statements.

The minimum required financial statement content is regulated by local GAAP or IFRS, depending on the framework that the company follows [21]. Financial statements comprise two parts: structured financial statements containing financial information and text explaining the financial information for fair presentation to users [22]; both parts are essential. The structured form of financial statements contains at minimum a balance sheet and a P&L statement, and listed companies present at minimum statements of cash flow and changes in equity [23]. The text part of the financial statements contains at minimum notes and/or annual reports [24].

This study aims not only to evaluate the effect of a global financial crisis on the quality of financial statements but also to build a framework for further research on similar data from other parts of the world. Therefore, the scope of the data used and the research method and technique are simplified for easy replication of this research anywhere in the world using local data. Extending the size of the research sample is recommended; however, this research was conducted on a relatively small scale to enable its replication by academics (or students) whose laptops may only be capable of processing limited amounts of data and are unable to proceed with large structured query language (SQL) databases locally.

Between 2020 and 2023, the global economy was affected by an unexpected crisis caused by the COVID-19 pandemic [25], which affected the transportation of people and goods [26], manufacturing and global supply chains [27], and everyday operations of companies and individuals worldwide [28]. For instance, COVID-19 disease prevention measures [29] contributed to the chip crisis [30], and the supply chain breakage contributed to inflation in 2024 [31]. Examination of financial statements from the periods before and after the pandemic provides relevant information from the real market. The global COVID-19 pandemic provides a unique opportunity to examine how a global economic crisis affected the behavior of companies in terms of their financial statement quality.

Hypothesis DevelopmentIn Slovakia, all enterprises, regardless of their size, must disclose their financial statements in the public financial statement database. The public database of financial statements is run by the Slovak government. All financial statements submitted to the public database of financial statements are freely accessible on the official website of the public database of financial statements. Such government conduct provides public oversight even for non-audited enterprises. An enterprise that fails to submit its financial statements to the public database of financial statements for two consecutive periods faces penalization by dissolution ex-officio. As financial statement disclosure is mandatory for Slovak enterprises, they are obliged to disclose their financial position not only to their investors, but also to all their business partners and interested parties. Other than investors, certain financial statement users are also obliged to analyze the financial statements of their business partners. The quality of the financial statements should be profound in order for users to receive legitimate information. Financial crises affect enterprises’ operations but should not affect the quality of their financial statements. The regulatory framework of financial statements should not be affected. Enterprises follow the same regulatory framework of financial statement regardless of the economic cycle. This theoretical assumption led us to verify our research hypothesis.

Hypothesis (H1). A global financial crisis does not affect the quality of figures disclosed in the structured parts of financial statements disclosed according to local GAAP.

Listed and large enterprises are subject to statutory audits. However, the main purpose of an audit is to assure users that financial statements provide fair presentation. A fair presentation is achieved when IFRS or local GAAP standards are met. IFRS allow enterprises to apply their subjective best estimates; for example, one enterprise uses a 2% discount rate to calculate the present value, and another uses a 4.7% discount rate to calculate the present value. Both are in the same reporting period and have the same obligations. Both enterprises inform the users of their financial statements about the discount rate they apply. However, enterprises that use lower discount rates incur higher costs in the current period. We do not instantly assume that the enterprises deliberately mislead users about their financial statements, as enterprises disclose their figures in a way that better fits their aims. Experienced users of financial statements are aware of such nuances that must be considered in the financial analysis process.

Hypothesis (H2). IFRS for financial statements quality of disclosed figures on structured financial statement forms is not affected by a global economic crisis.

IFRS are applicable regardless of the economic cycle. Enterprises follow the same methodology and rules during both recessions and expansions. Therefore, we assume no difference in the quality of financial statements among different economic cycle periods. The balance sheet and P&L statements must disclose the same fairness regardless of the economic cycle status. Companies’ operations are affected by the economic cycle; however, the quality of their financial statements must follow the consistency principle.

European directive 2013/34/EU on the annual financial statements consolidated financial statements and related reports of certain types of undertakings divides enterprises into four categories based on size of the enterprises: micro, small, medium-sized, and large enterprises. EU Member States are allowed to merge medium and large enterprises into a single category. In Slovakia, the Accounting Act considers only three categories of enterprises: micro, small, and large enterprises. Each size group is required to disclose different minimum requirements in their financial statements. Micro enterprises are exempt from several disclosures, such as deferrals or the fair value of financial assets and liabilities, but micro enterprises are allowed to voluntarily disclose their financial statements as small enterprises. A separate fourth group of enterprises disclose their financial statements according to IFRS. As the size of the enterprise increases, the requirements for disclosure in their financial statements also increase. The Accounting Act in Slovakia rigorously instructs enterprises on how to perform their accounting to achieve fair presentation in their financial statements. Slovak GAAP have not been introduced as stand-alone accounting rules but have been substantiated by European continental accounting GAAP, mainly by the Germany and France [32]. Slovak enterprises must follow EU directives as transposed into Slovakian legislation. Therefore, research on Slovak financial statement data is relevant. Further, the results are applicable beyond national borders, as the Accounting Act in Slovakia requires the application of generic accounting principles used worldwide and inspired by IFRS and EU directives [33].

From the more than 200,000 financial statements submitted for 2020 in Slovakia, we randomly selected four samples, each represented by the financial statements of its size group: micro enterprises, small enterprises, large enterprises, and enterprises disclosing financial statements according to IFRS. Each sample contained 100 randomly selected financial statements submitted for the financial year ending in 2020. To ensure that all samples were selected randomly, we used a random number generator that aligned a random number to each financial statement. We then sorted all financial statements according to the aligned random numbers and filtered the financial statements for each size group. First, 100 financial statements were selected. For each sample, we manually checked all the financial statements and excluded those that were not disclosed according to the going concern principle—financial statements that disclosed the enterprise’s dissolution date. From the sample of IFRS statements, we excluded financial statements from financial and insurance enterprises, as financial and insurance enterprises follow industry-specific, more scrutinized requirements for disclosures, affected by special legislation applicable only to financial institutions, such as BASEL 3 or SOLVENCY 2, and similar legal requirements. Therefore, financial institutions are not suitable for our research, especially considering that we compared enterprises of different sizes and businesses affected mostly by similar disclosure requirements.

To evaluate the quality of financial statements after the crisis, we chose financial statements from the financial year ending in 2023 for the same enterprises from which those for the financial year ending in 2020 were chosen. Comparing financial statements from the beginning of the financial crisis to those from the end of the crisis provides an overview of how the crisis affected companies of different sizes in Slovakia. To determine whether the global economic crisis affected the quality of the reported financial statement figures, we build regression models on four random samples, with each sample representing a company size category. Based on a comparison of results gained from the two distinguished periods, we can determine the financial crisis’s impact on the quality of financial statements for each sample. We examine the usefulness of published financial statements using standardized financial indicators: Return on Assets (hereinafter referred to as ROA), Return on Equity (hereinafter referred to as ROE), The Quick Ratio (hereinafter referred to as QR), Revenue Growth Rate (hereinafter referred to as RG), the Debt-to-equity ratio (hereinafter referred to as DER), and the Current Ratio (hereinafter referred to as CR) [34]. The choice of indicators, as well as their use and research, is based on the practices described in the scientific literature and a high degree of standardized use [35]. In this study, we prefer to use generally accepted and recognized financial analysis indicators. The main idea is not to build a stochastic model, but to compare statistical performance between the two distinguished periods. We expect the statistical indicators to be similar for both periods for each sample group. The indicators used in this research are built on ratios. This approach ensures that even if the market moves in any direction, the ratios shall maintain the same or similar form. To eliminate industry specifics and other external influences that may affect financial ratios, we use random samples containing financial statements from any industries, so that individual effects will be smoothed out. We emphasize that individual or an industry-specific effects cannot be fully eliminated, yet the research can be easily replicated using different sample or an extended sample in order to verify the result of the research.

Currently, the trend is to adopt machine learning tools using a neural network [36]. Modern tools based on artificial intelligence are undoubtedly a future trend and are worthy of independent research. The publicly available AI tools currently exhibit substantial errors [37]. A neural network-based model requires considerable data for training [38]. As the objective of this study is not to explore machine learning methods using a neural network, we prefer traditional research methods and tools. We use traditional methods over modern ones because of their informational ability to compare the standardized indicators used and the comprehensibility of the methods used. This provides the opportunity for independent researchers to verify the research results at any time or to replicate this research domestically using local data.

The selection of indicators as independent variables is based on the academic literature. Therefore, we do not advocate the relevance of the variables selected in this study. The financial indicators used in this study are standardized tools used in the financial analysis of data from the structured forms of financial statements of individual size categories of enterprises. With an appropriate selection of different financial indicators, we should obtain similar results regarding the ordinal usefulness [39] of the financial statements of individual size categories of enterprises. The different financial indicators provide different results in the subsequent regression analyses. Despite the different regression analysis results, the ordinal usefulness of the financial statements of individual size categories of enterprises should be maintained. Therefore, we do not focus deeper on the financial indicators used in this research; instead, we focus on the academic literature, such as [35,40–42], among others.

As in [7], the informational relevance of individual indicators is evaluated based on an assessment of the validation of the data published in the financial statements and shareholder returns. To test the relationship between indicators as independent variables and shareholder returns as a dependent variable, we use three models inspired by valuation theory research [43,44]:

The first model is based on the classic financial analysis indicators of an entity’s performance. The second is based on an analysis of the entity's assets and liabilities. The third model is based on financial performance indicators and the enterprise’s asset-liability structure.

We conduct research using data from the financial statements of enterprises in Slovakia for the accounting period ending in 2020. Most enterprises apply an accounting period that is identical to the calendar year. For enterprises that apply the accounting period of the financial year, we use financial statements prepared for the financial year ending in the calendar year 2020. We compared the research results obtained using data on the financial statements from 2020 with the same data of the same enterprises in the same-size samples from 2023. By comparing the research results from 2020, the beginning of the COVID-19 pandemic, to those from 2023, the period after the COVID-19 pandemic, we can adjust the possible conclusions regarding the pandemic’s theoretical impact on the data reported in the financial statements. Regarding the theory of large numbers [45] and the universal application of IFRS and Slovak accounting legislation to Slovak enterprises, we assume that the COVID-19 pandemic and its impact on the national economy will not affect the regression analysis results used to evaluate the ordinal usefulness of the data published in the balance sheets and P&L statements. To minimize doubts about the research results, we chose two relatively separate periods, and each of the selected accounting periods is characterized by a different economic environment in which the enterprises operate. Year 2020 is characterized by the consequences of the ongoing global pandemic, and 2023 is characterized by the recovery of the global economy after the COVID-19 pandemic [46]. The theoretical assumption that the research results are independent from the economic and financial fluctuations of the world economy is verified by comparing the results of the regression analysis on data from the beginning of the COVID-19 pandemic and data from the end of the COVID-19 pandemic. We expect the same results for the ordinal usefulness of a fair presentation of financial information in financial statements regardless of the reporting period.

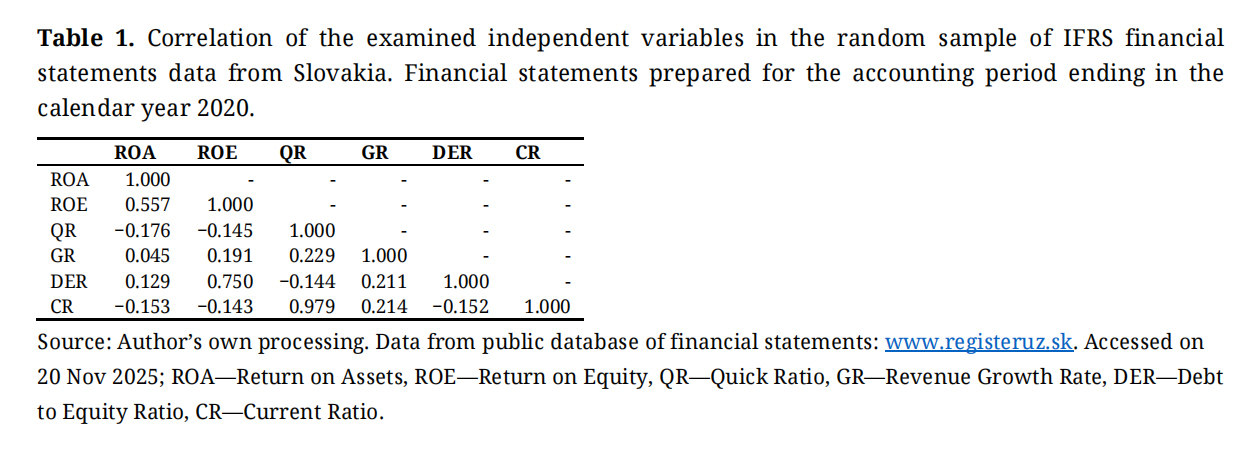

When modeling a dependent variable using independent variables, it is essential that the individual variables are independent of each other. The basic tool is study of the correlation between individual variables. Based on the results of this correlation, we either adjust the selection of the input variables or select a suitable regression model. Table 1 presents the correlation of the examined variables from the sample of IFRS financial statements for the financial year ending 2020. A significant correlation is observed between the CR and the QR. A higher correlation between the CR and the QR is expected given the common denominator, which is the value of short-term liabilities. If the correlation is close to 1, it is necessary to exclude the variables from the model. In the four random samples studied, we observe a significant correlation between the CR and QR variables.

Table 1. Correlation of the examined independent variables in the random sample of IFRS financial statements data from Slovakia. Financial statements prepared for the accounting period ending in the calendar year 2020.

Table 1. Correlation of the examined independent variables in the random sample of IFRS financial statements data from Slovakia. Financial statements prepared for the accounting period ending in the calendar year 2020.

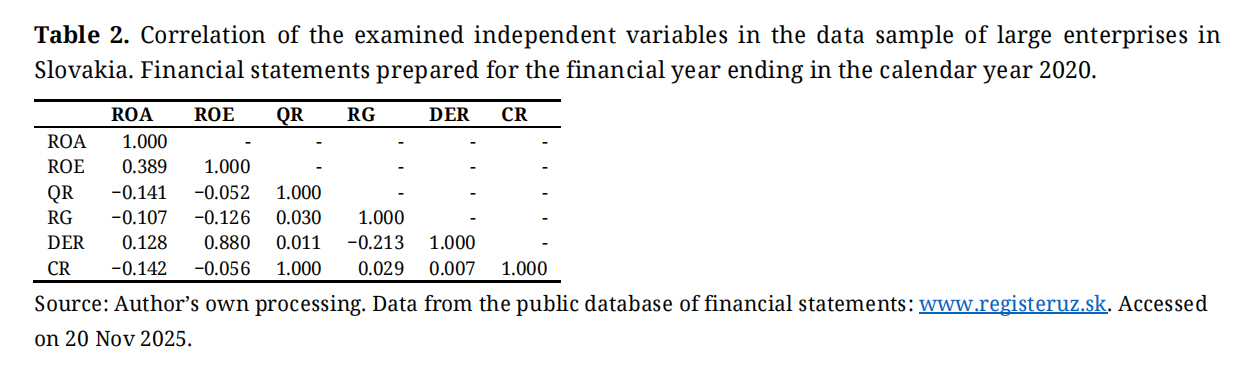

In the samples of the financial statements of large (Table 2), small (Table 3), and micro (Table 4) enterprises, we observe a significant correlation between the ROE and the DER. For IFRS financial statements, we do not observe a significant correlation between the ROE and the DER. Both variables have equity in the denominator. Therefore, a certain degree of correlation is expected between them. The subsequent sections present a deeper examination of the possible reasons why a sample of financial statements compiled according to IFRS shows a significantly different degree of correlation between ROE and DER; we expect a consistency of correlation across individual samples.

Table 2. Correlation of the examined independent variables in the data sample of large enterprises in Slovakia. Financial statements prepared for the financial year ending in the calendar year 2020.

Table 2. Correlation of the examined independent variables in the data sample of large enterprises in Slovakia. Financial statements prepared for the financial year ending in the calendar year 2020.

The examined financial statements of large, small, and micro enterprises are compiled based on the results of accounting maintained according to the Slovak legislation. Micro enterprises have simplified legislation for the preparation of financial statements, and they maintain accounts according to the same law and measure of the Ministry of Finance as small and large enterprises. The following sections present deeper examinations into the causes of possible differences in the results of the correlation of financial analysis variables obtained from data in financial statements prepared according to Slovak accounting legislation and those prepared according to IFRS. They will be discussed later.

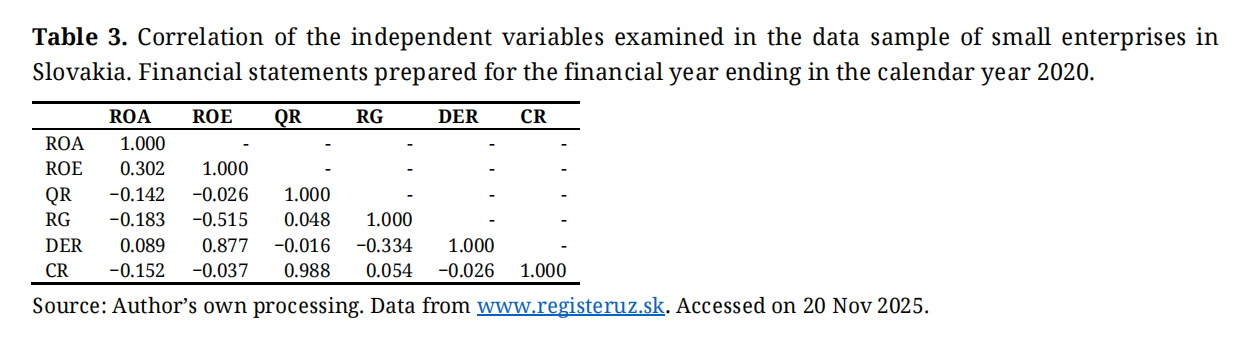

Table 3. Correlation of the independent variables examined in the data sample of small enterprises in Slovakia. Financial statements prepared for the financial year ending in the calendar year 2020.

Table 3. Correlation of the independent variables examined in the data sample of small enterprises in Slovakia. Financial statements prepared for the financial year ending in the calendar year 2020.

In general, the examined variables can be considered relatively suitable for further modeling, with a high correlation between the QR and the CR of more than 0.80. We build regression models using several variables and their combinations; thus, despite the high correlation between the two variables, the research continued because we considered the higher correlation when interpreting the regression analysis results. We do not aim to build a stochastic model; rather, we examine the ordinal usefulness of financial statements for analyzing the effect of a financial crisis on the quality of the figures presented in the financial statements.

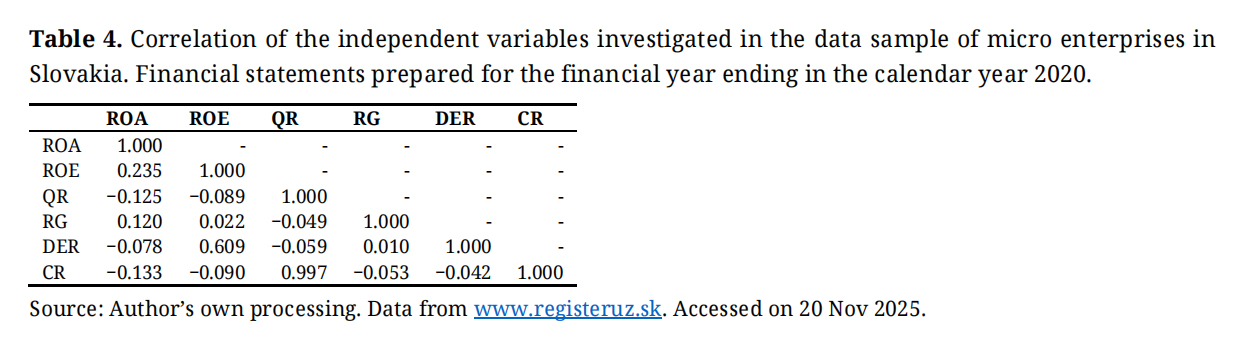

Table 4. Correlation of the independent variables investigated in the data sample of micro enterprises in Slovakia. Financial statements prepared for the financial year ending in the calendar year 2020.

Table 4. Correlation of the independent variables investigated in the data sample of micro enterprises in Slovakia. Financial statements prepared for the financial year ending in the calendar year 2020.

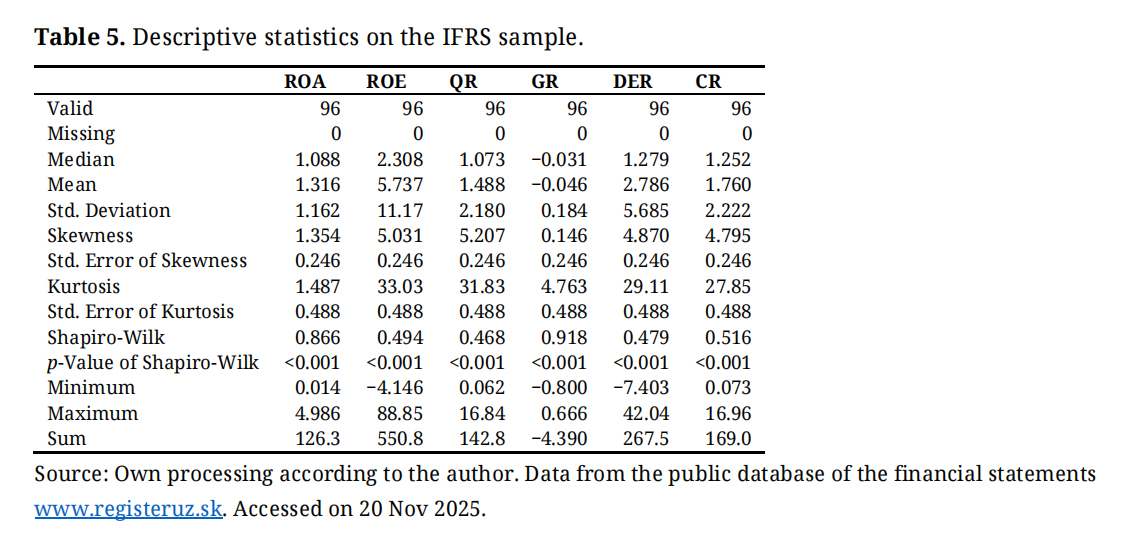

Table 5 shows the descriptive statistics results of a randomly selected sample of companies preparing their IFRS financial statements for the accounting period ending in the calendar year 2020. A difference between the mean and median is observed for all examined indicators, with the smallest absolute difference between the mean and median being for the RG indicator. The coefficient of asymmetry—Skewness—is “close” to zero only for the GR indicator.

Table 5. Descriptive statistics on the IFRS sample.

Table 5. Descriptive statistics on the IFRS sample.

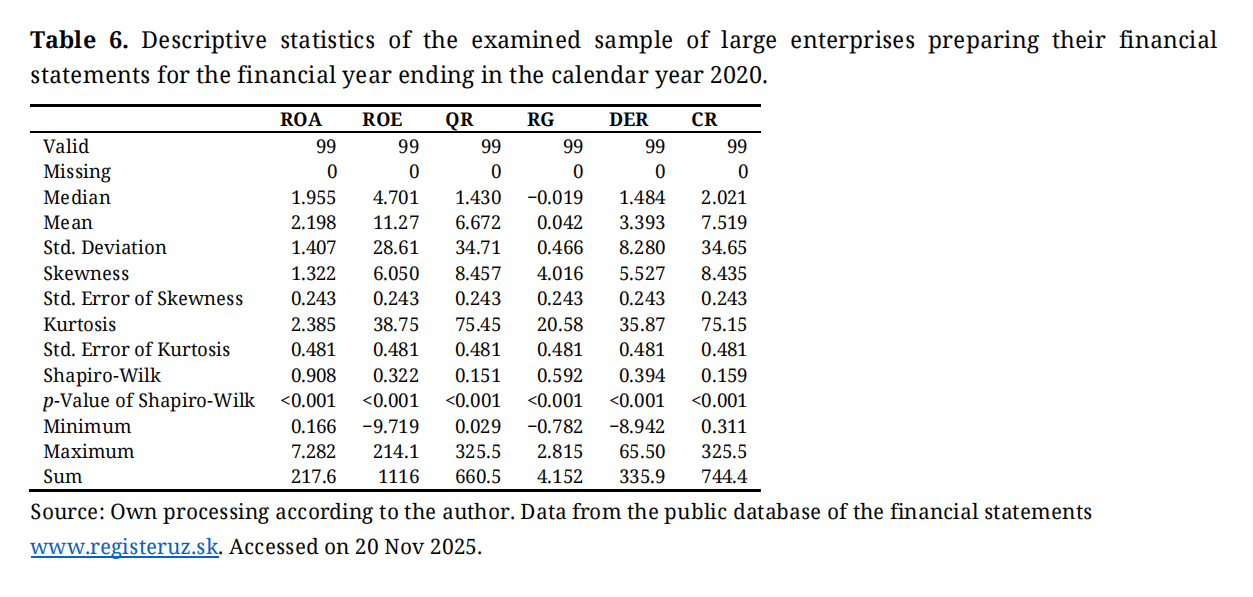

When comparing the descriptive statistics of the sample of large enterprises (Table 6), we observe values with a relatively small difference between the mean and median for the same indicators as in the sample of financial statements of enterprises prepared according to IFRS. As in the IFRS sample, the asymmetry coefficient was close to zero only for the GR indicator.

Table 6. Descriptive statistics of the examined sample of large enterprises preparing their financial statements for the financial year ending in the calendar year 2020.

Table 6. Descriptive statistics of the examined sample of large enterprises preparing their financial statements for the financial year ending in the calendar year 2020.

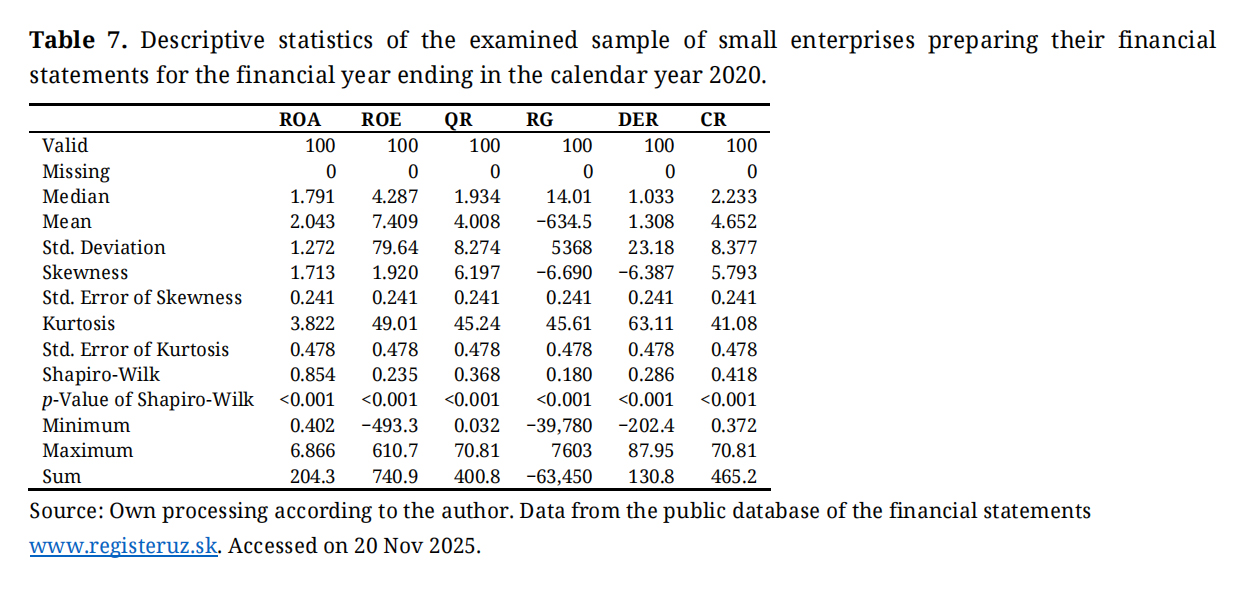

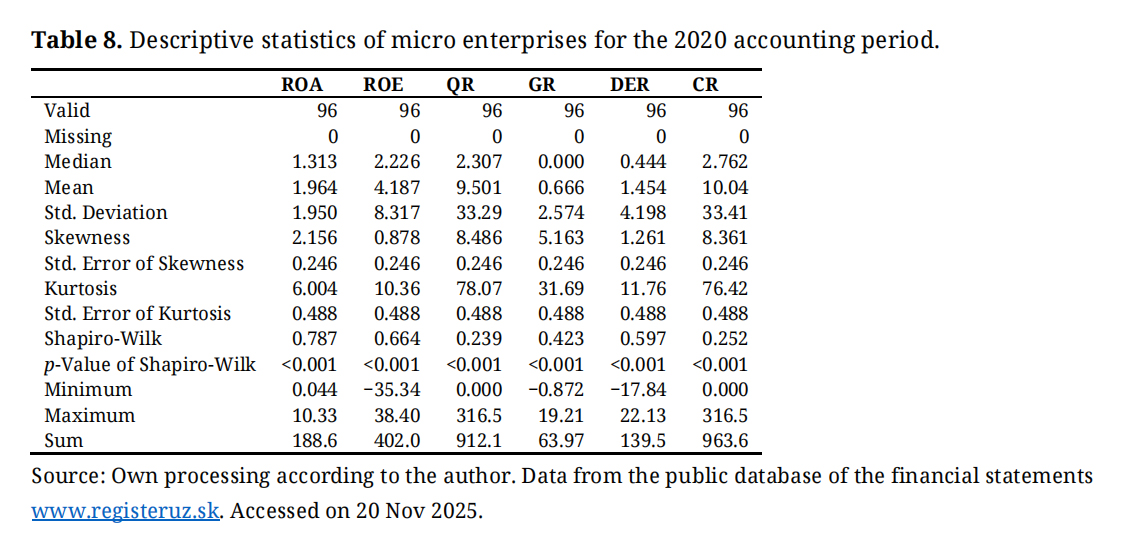

By examining the descriptive statistics of the indicators on the samples of small enterprises (Table 7) and micro enterprises (Table 8), we observe how the homogeneity of individual samples gradually decreases with decreasing enterprise size as well as the difference between the mean and the median and the asymmetry coefficient, among others.

Table 7. Descriptive statistics of the examined sample of small enterprises preparing their financial statements for the financial year ending in the calendar year 2020.

Table 7. Descriptive statistics of the examined sample of small enterprises preparing their financial statements for the financial year ending in the calendar year 2020.

Table 8. Descriptive statistics of micro enterprises for the 2020 accounting period.

Table 8. Descriptive statistics of micro enterprises for the 2020 accounting period.

The micro enterprise sample is the least homogeneous of the four samples examined. Enterprises’ financial statements represent a random selection of business entities operating in different sectors and facing different microeconomic circumstances. The entities operate in the same global market; however, their financial analysis indicators cannot be assumed to have a normal distribution. If this were the case, it would imply a significant degree of uniformity in the business environment or subjectivity in the sample selection.

Better informative power can be achieved by expanding the sample of individual enterprise types; however, this study does not aim to provide an exhaustive analysis of the entire Slovak market represented by all enterprises. The examined samples are selected randomly. Statistical information from the examined samples can be considered sufficient for research on the ordinal usefulness of the financial statements of individual size categories of enterprises [47]. Owing to the relative simplicity of the research methodology and the relatively accessible possibility of repeating the research on another random sample by an independent researcher or on a sample of data from another country, the research results have applicable impact, as the conclusions can be applied beyond the borders of Slovakia.

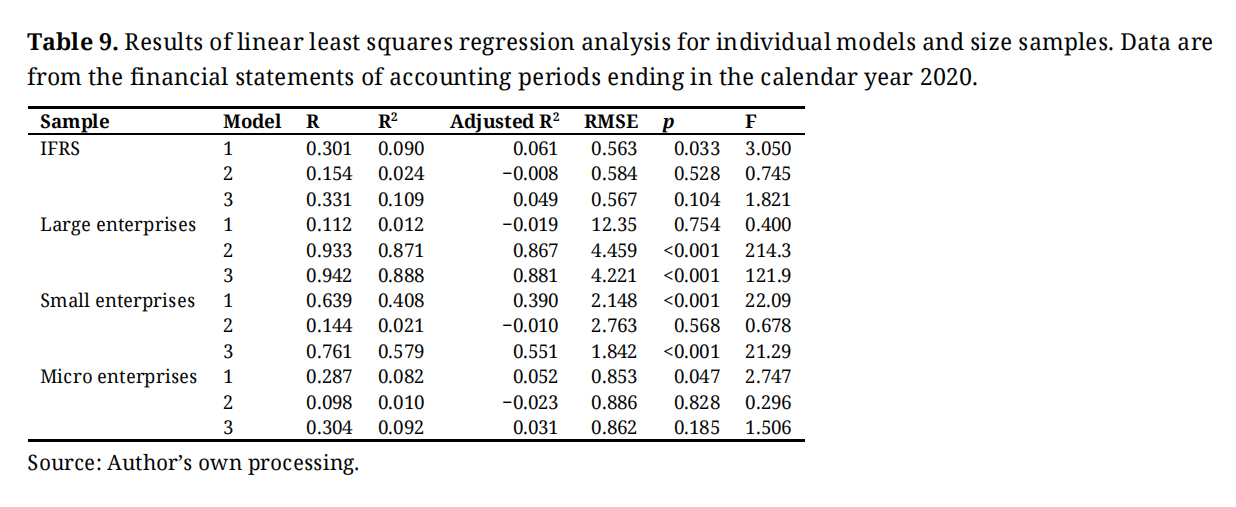

Regression AnalysisWe gradually build individual models on all four samples of enterprises using software: Gretl, version 2025a, copyright 2000–2020 Allin Cottrell and Riccardo “Jack” Lucchetti; JASP, version 0.95.4, copyright 2013–2025 University of Amsterdam; Excel, version 16.103.3, copyright Microsoft 2025. Table 9 lists the basic indicators for each linear regression model. The coefficient of determination (R2) provides the smallest values for the micro enterprises sample. For micro enterprises, the coefficient of determination provides the highest value [35].

Table 9. Results of linear least squares regression analysis for individual models and size samples. Data are from the financial statements of accounting periods ending in the calendar year 2020.

Table 9. Results of linear least squares regression analysis for individual models and size samples. Data are from the financial statements of accounting periods ending in the calendar year 2020.

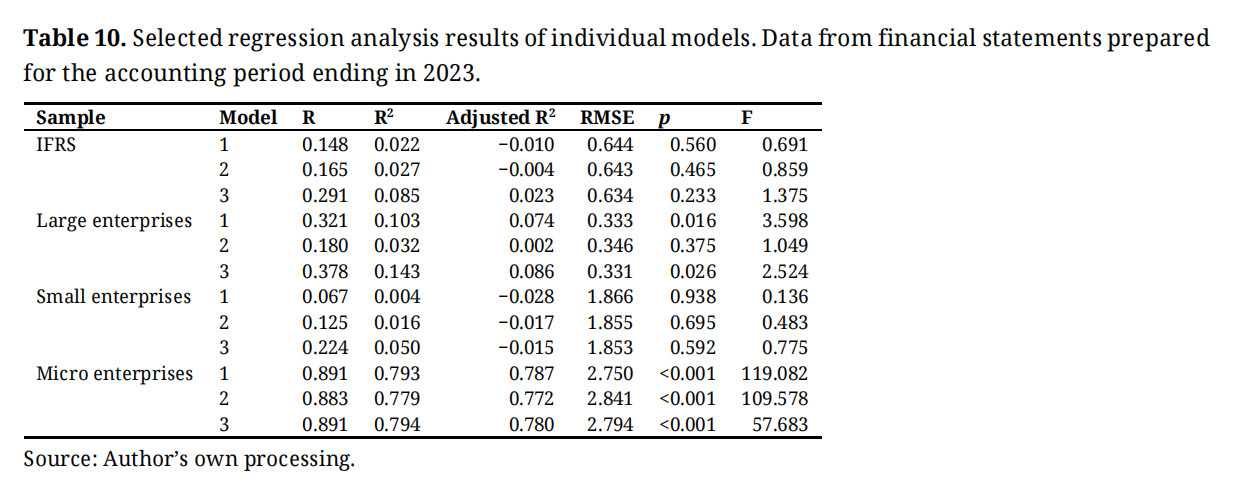

To evaluate the results, it is necessary to verify whether they are similar to those obtained using the sample of financial statements from 2020 in another monitored period. Random size samples from the previous part of the research contained financial statements for the accounting period ending in 2020, that is, the first year of the COVID-19 pandemic [25]. To confirm or refute the original findings of the research, we used a sample of the same enterprises as in 2020 but for 2023. We do not evaluate the statistics of the number of defaulted enterprises during the COVID-19 pandemic or the impact of the COVID-19 pandemic on the health of enterprises, nor do we intend to formulate conclusions in connection with the COVID-19 pandemic; rather, we refer to the academic literature, for example [48]. Table 10 shows selected results for linear regression models on samples of the same enterprises, but from financial statements for the accounting period ending in 2023, that is after the COVID-19 pandemic had subsided.

Table 10. Selected regression analysis results of individual models. Data from financial statements prepared for the accounting period ending in 2023.

Table 10. Selected regression analysis results of individual models. Data from financial statements prepared for the accounting period ending in 2023.

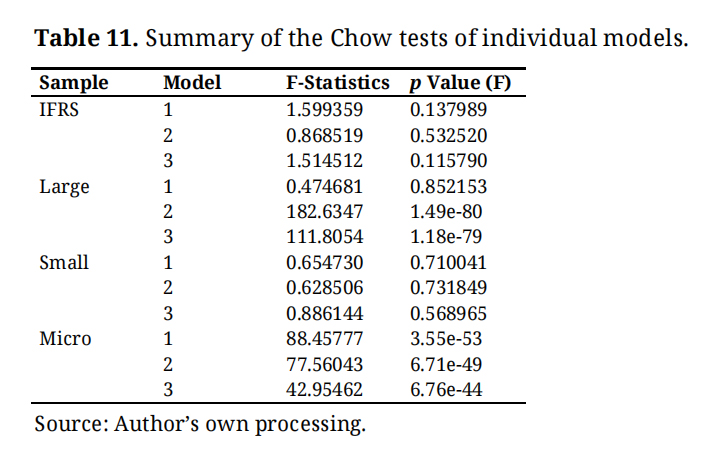

Research on samples from both 2020 and 2023 confirms that micro enterprises have the best predictive ability for facilitating financial analysis of data in the structured parts of the financial statements. To compare regression analysis results between two observed periods, we apply Chow test (Table 11) for all samples and models.

Table 11. Summary of the Chow tests of individual models.

Table 11. Summary of the Chow tests of individual models.

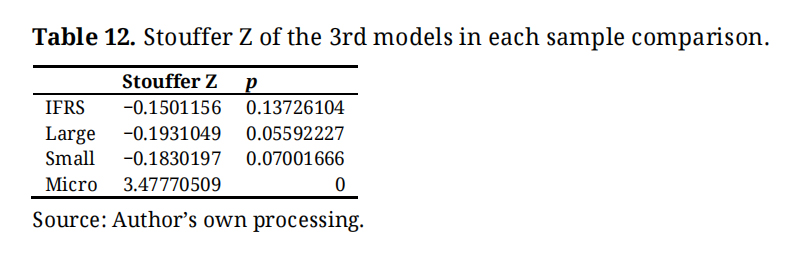

Except of models built on micro enterprises data, all other models are showing p Value more than 0.05. We have detected structural changes in the models based on local GAAP data, among the two distinct examined periods, only for micro enterprises and partially for large enterprises. Our original assumption was that the results shall remain regardless the period. We have taken samples from the year 2020 of recession and from the year 2023 which represents expansion. We expected the results of the regression analysis similar as the economic cycle effects shall affect both independent variables and dependent variable. We have found out the economic cycle affects the quality of the results in the financial statements. To figure out how economic cycle affects the quality of the financial statements in each type of companies, we calculate Stouffer Z [49] in Table 12.

Table 12. Stouffer Z of the 3rd models in each sample comparison.

Table 12. Stouffer Z of the 3rd models in each sample comparison.

By comparing the regression analysis results of the samples of financial statements from 2020 and 2023, we observe the following:

●

●

●

●

Based on the results of this study, the quality of the information presented in financial statements in Slovakia is acyclical for financial statements prepared in line with IFRS and for the financial statements of small enterprises. The IFRS is a uniform and precisely defined methodology for preparing financial statements. According to Slovak accounting legislation, micro, small and large enterprises comply with the precisely defined rules from accounting legislation in Slovakia prepare their financial statements according to a precisely defined uniform methodology. Financial statements prepared according to IFRS and financial statements of small enterprises provide the same quality of information, regardless of the global economic fluctuation caused by, for example, the financial crisis or the COVID-19 pandemic. In this study, we confirmed our hypothesis H2, as the global economic crisis had no significant impact on the quality of IFRS financial statements. We can state that the IFRS financial statements and the financial statements of small enterprises maintain the same fairness of their financial statement presentation, regardless of global financial circumstances. In spite of H2, we confirmed that global economic crises affect the quality of the financial statements of large and micro enterprises; the quality of financial statements of large enterprises is contercyclical, and the quality of financial statements of micro enterprises is cyclical. We reject H1, as the financial crisis affected the quality of financial statements for some legally determined size groups.

Result of this study could be improved by extending the sample observations. Sample of approximately 100 observations is enough, especially considering randomness of the selection. Despite of random selection some external effects such as industry specifics or non-financial effects could affect the results of the research. Such influences could have been smoothed out by extending the samples or by replicating the research on different samples. We are aware of the limitations of this research. We encourage other researcher to get inspired by this research and to perform their own research on financial statement data.

Through financial analysis and mutual comparison of results between legally determined size categories of enterprises in Slovakia, we demonstrated a higher usefulness of the presented financial data in the balance sheet and the P&L statements of enterprises that prepare their financial statements according to the Slovak accounting regulation compared to financial statements prepared according to IFRS. This does not affect the fairness of the data disclosed in the IFRS financial statements. With the gradual expansion of IFRS in a globalized environment [52], it is necessary to pay attention to the expertise [53] of financial statement users so that the data disclosed in financial statements prepared in accordance with IFRS can be correctly interpreted. However, this could not be achieved without human intervention. For tax purposes, clear and uniform rules are necessary so that the subjective judgment of enterprises does not lead to distortion of accounting records [54], and thus, to distortion of the economic result. The profit disclosed in a financial statement is used to determine profit tax; it must be among the highest interests of tax administrations to ensure that enterprises determine their profit before taxation fairly [55]. Knowledge of how the economic cycle might affect the fairness of financial statement disclosures is important for examining whether the disclosed financial statement figures are the result of an enterprise’s performance alone or whether the disclosed figure might be affected by enterprise management, regardless of their motives, or affected by the rigid GAAP. Further academic research and academic discussion is needed to figure out whether principle-based GAAP, such as IFRS, or more scrutinized GAAP, such as those used for micro enterprises in Slovakia, are useful for the users of the financial statements. IFRS is aimed at financial statement users from among the capital market participants [17]. Yet there are others significant groups of financial statement users, such as those looking for aggregated financial statement data for macroeconomic analysis [56], or those looking for specific ratios, such as market regulators, financial institutions, etc. As shown in this research, both extremes—principle-based IFRS and heavily scrutinized micro enterprise’s GAAP—showed the acyclicity of their financial statement quality. Micro and large enterprises, with obligations to disclose information in their financial statements between extreme scrutiny and principle-based GAAP, are vulnerable to the quality of their financial statements regarding the economic cycle. Each enterprise is responsible for its own financial statement, yet policymakers and regulators are able to determine market or industry performance based on aggregated data. If the disclosed data quality is affected by the economic cycle, the user of the financial statement will notice. Or policymakers will establish GAAP that maintain the quality of financial statements regardless of the economic cycle. As national GAAP are influenced by global accounting trends, a broader global academic discussion is needed. Further accounting research on the evaluation of accounting trends is welcome; despite global IFRS adoption, academics will not remain mere trend evaluators but will use the concentration of knowledge to become accounting trend setters.

When analyzing financial statements, the trend is to use machine learning and automation tools [57] to evaluate the information in the text part of financial statements together with disclosed figures in the structured parts of financial statements. In addition to presenting financial information, this is also coming to the fore, especially in terms of DEI and environmental sustainability [58]. This gives the non-financial part of the financial statements significant importance, along with the financial part of the financial statements. The achievement and reporting of the climate objectives of the Green Deal [59] are being put on an equal footing with useful information on the financial and asset health of enterprises disclosed in traditionally used balance sheets and P&L. Despite the increasing importance of non-financial information being disclosed in financial statements, it is still important to disclose the financial sustainability of enterprise operations. Investors and users of financial statements use the balance sheet, P&L, and cash flow statements to find the most important information for financial analysis. It is therefore important to know how the quality of the disclosed information in a balance sheet and P&L is affected by the global economic crisis, and whether and to what extent enterprises tend to embellish their financial statements [60] with regard to the economic cycle.

This study’s results confirm those of other authors examining a different economic crisis in 2007–2008 on comparable markets—Italy and the Eastern European region [50,51]. The confirmation of such results in other periods or other markets indicates the universal application of the results of this research for further interpretation of the results of financial analysis. Policymakers may also use the results of this study to shape the requirements to be disclosed in the financial statements of different enterprise size groups. Requirements for disclosure in financial statements have been extended over time [61], yet it is necessary to know whether and to what extent the disclosed information is being affected by external elements, such as a global economic crisis [62].

As the results that enterprises disclosed in their financial statements may be used in their aggregated form for macroeconomic analysis [63], the results of this study provide direct information for macroeconomic analysis. The cyclicity and countercyclicity of large enterprises and cyclicity of micro enterprises regarding the quality of disclosed figures in balance sheet and P&L statements may be determined in further adjustments to policymaking and regulatory requirements. Further research and broader academic discussion on this topic are needed to improve the global business environment. The result of this research being determined by traditional statistical methodology should be compared by further research, especially research using modern tools based on machine learning and AI. We encourage academics to further extend this research, to challenge this research and to share their own research on accounting to enrich scientific knowledge and to contribute to better business sustainability reporting.

All data used in the study are available in the public database of Slovak financial statements on www.registeruz.sk.

Conceptualization, JV and JM; methodology, JV and JM; validation, JV and JM; writing—original draft preparation, JV; writing—review and editing, JV and JM; visualization, JV; supervision, JM.

The authors declare no conflicts of interest.

Not available.

This paper is result of VEGA project No. 1/0497/25, Implementation of innovative approaches in the field of risk management and modeling within the internal models of insurance companies.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

Vlčko J, Meluchová J. Impact of a global economic crisis on balance sheet and P&L quality: Evidence from Slovakia. J Sustain Res. 2025;7(4):e250073. https://doi.org/10.20900/jsr20250073.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions